Key takeaways

- Personal liability insurance pays for personal injury, property damage, and financial losses that you have caused to others. You have to bear these costs if you don’t have private liability insurance. The claims against you can get expensive, especially if you hurt people.

- A good private liability insurance also steps in if someone else causes you damage.

- Personal liability insurance fends off unjustified claims against you.

- If you are a student, your parents’ private liability insurance covers you – even if you no longer live with them.

This is how you do it

- Take out personal liability insurance if you don’t have one. You can get a good liability insurance cover for under 100 € a year.

- You can save money by changing your private liability insurance contract every year. New contracts often offer better benefits. So keep an eye on your termination date. If your insurer increases the premium without improving the benefits, you can cancel the contract immediately in Germany.

- You can get personal liability insurance policies via comparison portals like Check24* and Verivox*. We find the liability insurance plan from Die Haftpflichtkasse (Einfach Komplett) the best.

Table of Contents

Personal Liability Insurance, commonly known as “Haftpflichtversicherung” in German, is a crucial safety net that shields you from the potential financial burdens arising from unintentional harm caused to third parties.

In this guide, you’ll learn about the ins and outs of German Personal Liability Insurance. Hence, it empowers you to make informed decisions that protect both your interests and others.

What is covered under Personal Liability Insurance Germany (Haftpflichtversicherung)?

Personal liability insurance covers the costs if you accidentally break something or injure someone. Its coverage can be divided into three broad categories.

- personal injury,

- property damage,

- and financial loss.

For example, a motorist falls because of you. As a result, the motorist was hospitalized and later spent several weeks in rehabilitation.

In the above case, you pay for the following damages

- compensation for pain and suffering (personal injury)

- medical costs

- the motorist’s loss of earnings (financial loss) as they cannot work

- motor cycle repairs (property damage)

In the worst-case scenario, suppose the motorist dies because of your fault. The damage claims can be in the millions, which could lead to your personal bankruptcy.

You are liable for the damage caused – up to your personal seizure limit (Pfändungsgrenzen in German).

People use the terms personal liability insurance, private liability insurance, and third-party liability insurance interchangeably to describe the same insurance type.

Since no one can foresee accidents, everyone should have personal liability insurance in Germany. Moreover, it can protect you from personal bankruptcy.

Examples of when personal liability insurance covers damages

| Damage Type | Example | Costs | Approx. Damage Amount |

|---|---|---|---|

| Personal injury | You open the door of your car without looking behind, and a cyclist crashes into it. The cyclist hits the road with his head. As a result, the cyclist is paralyzed and cannot work anymore. | The cyclist’s family demands compensation for the accident, including monthly care costs. | The cost can go as high as 8 million euros |

| Property damage | Your son burned some paper in the school, which led to the burning of part of the school building. | You are held liable to pay for sanitation and repair costs. | approx. 10 million euros |

| Financial loss | You are smoking a cigarette and accidentally set the garbage near a restaurant on fire. Because of the smoke, many guests leave the nearby restaurant. | The restaurant owner claims financial losses because of the reduced sales. | 300 € to 1000 € |

| Lost keys | You lose the key to your rented apartment. As there are commercial shops in the rental property, the central locking system has to be replaced. | The landlord claims the costs of replacing the locking system. | up to 10,000 € |

| Lost keys (office) | You lost your key or card to access your office building. | Your employer demands the costs of replacing the locking system or creating a new card. | 500 € to 1000 € |

| Rental property damage | You accidentally burn the kitchen slab of your rented apartment by putting a hot utensil on it. | The landlord claims the cost of replacing the kitchen slab. | 150 € to 300 € |

| Damage to borrowed or rented items | You borrowed a drill machine from your friend, which fell and cannot be repaired. | You file a claim with your liability insurance provider to compensate your friend. | 100 € |

| Damages while helping a friend | You mistakenly drop your friend’s television while helping them move into a new apartment. | Your friend requested a replacement. | 500 € to 1000 € |

What is not covered by private liability insurance in Germany?

Private liability insurance does not cover the following:

- Personal damage: Injuries to your own body that you (accidentally) inflict on yourself

- Intentionally caused damage

- Damage resulting from criminal offenses

- Fines and damages due to breach of contractual obligations

- Damages covered by car insurance

- Damages caused by your dogs

How do you report a liability incident to your private liability insurance provider?

If you have accidentally caused damage to a third party, you should check whether your personal liability insurance covers it. If it does, report the incident to your insurer immediately.

There is no hard deadline defined under law for reporting the liability incident, but it’s recommended that you inform your insurer within a week.

The liability insurer requires proper documentation of the accident when you report the damage.

Moreover, you should only state facts and refrain from making your own assessments. Verivox* has shared some “w-questions” to help you describe the course of events as completely as possible:

- When did the mishap happen?

- Where exactly did it happen?

- Who is the cause of the damage, and who is the injured party?

- What damage has occurred?

- How did the accident happen?

It is helpful to take pictures of the place where the accident occurred. On top of it, take photographs of broken items also.

Attach the photos with your accident report and email them to your insurance company.

Moreover, if you have additional information, like the original invoice for the damaged item, you should also submit a copy.

Mistakes to avoid while dealing with liability claims

You accidentally caused damage to someone. And you want to repair the damage as quickly as possible. But acting in haste can harm you financially.

Here are the two mistakes you should avoid while dealing with the damage you caused.

- Never pay the injured party from your pocket. You should let your personal liability insurance provider compensate the injured party. The reason is that you don’t know the exact compensation amount. Hence, if you paid more than the rightful compensation, you may not get back the difference.

- Never promise specific compensation. If you promise a specific compensation amount to the injured party, you put yourself at financial risk. The reason is that you might have to pay the difference if the insurance benefit is lower than what you promised.

Hence, it’s best to apologize for the accident and assure the injured party that you’ll contact your private liability insurer to settle the damages.

What to do if the liability insurance case goes to court?

Sometimes, the benefits your liability insurer offers do not meet the injured party’s expectations. Hence, the injured party may take the matter to court to sue for higher damages.

Don’t worry; your personal liability insurance company offers legal protection to defend you in court.

Moreover, the following principle applies under German law: As soon as private liability insurance takes over the case, direct claims for damages to the policyholder are no longer permissible.

How much does personal liability insurance cost in Germany?

Good private liability insurance is available for 50€ a year for a single person and for less than 100€ a year for families.

Various insurance companies differ in terms of contributions and benefits. Moreover, the most expensive tariffs do not necessarily have the best benefits.

The most important difference between liability insurance providers is

- The sum the insurance company pays in the event of damage (sum insured).

- The insured areas of life

- Whether you’ll get money if someone causes damage to you, but cannot pay for it.

So, it makes sense to compare private liability insurance companies and their tariffs.

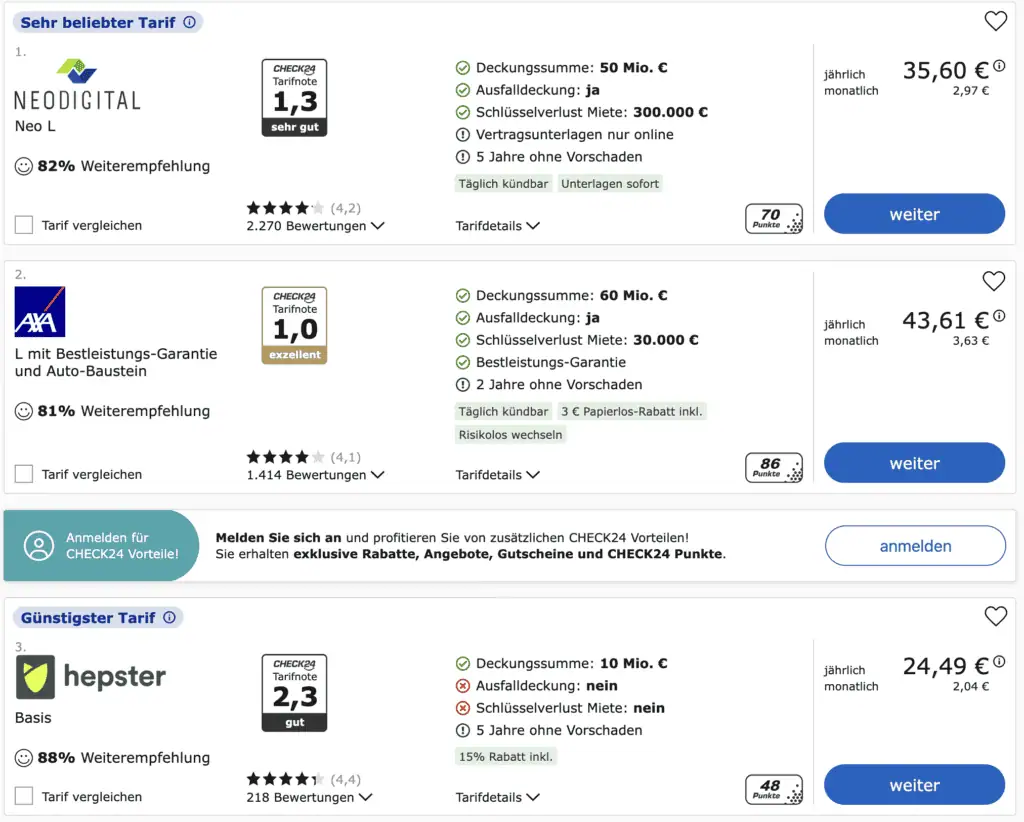

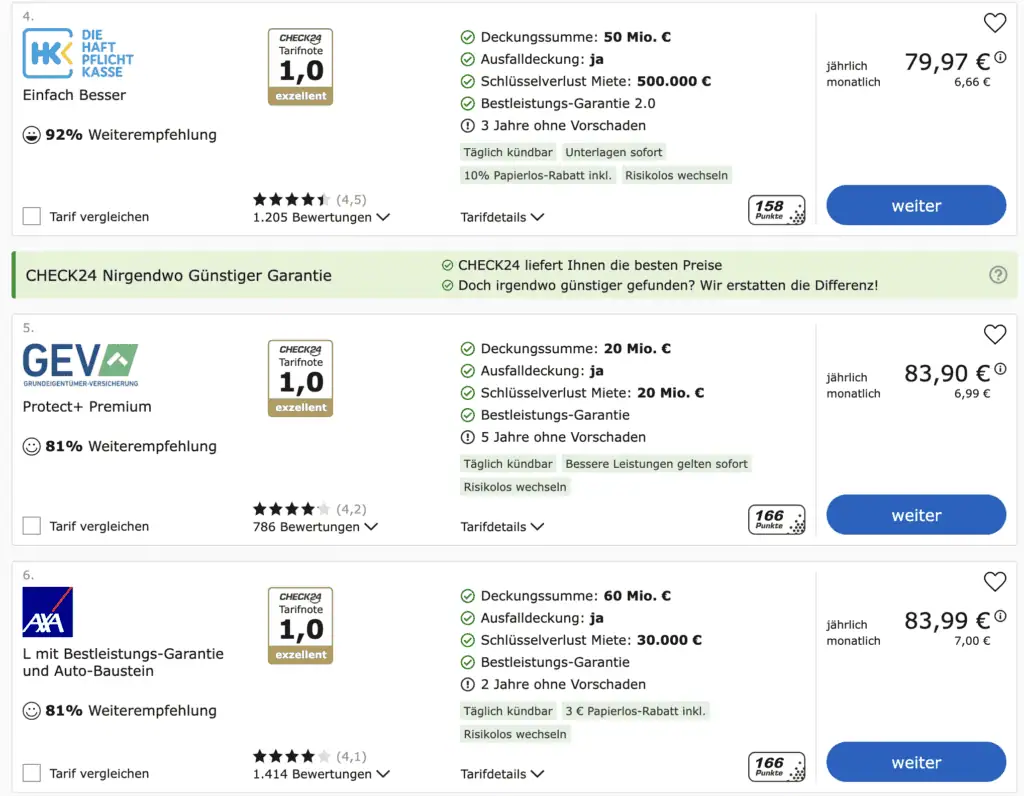

You can get personal liability insurance on comparison portals like Check24* and Verivox*. The personal liability insurance from “Die Haftpflichtkasse (Einfach Komplett)” is rated the best by all the rating agencies (Morgen & Morgen, Franke Bornberg, Stitftungs Warentest) and experts (Bierl, VMK, Finanztip).

Compare liability insurance on Tarifcheck

- Compare offers and prices.

- Comparison calculator to find the best liability insurance in Germany.

- Compare the insurance providers and their ratings.

Compare liability insurance on Verivox

- Compare offers and prices.

- Comparison calculator to find the best liability insurance in Germany.

- Compare the insurance providers and their ratings.

What should your personal liability insurance policy contain?

Here are the most important points you should consider when comparing personal liability insurance.

- High insured sum (Deckungssum)

- Bad debt (Forderungsausfall)

- The Best Performance Guarantee (Die Best-Leistungsgarantie)

- Best performance guarantee according to the GDV model conditions

- Deductible

- Lost keys

- Data exchange

High insured sum (Deckungssum)

Always pick the liability insurance tariff with the highest insured amount.

A higher insured sum costs a little more, but it’s worth it, especially if you accidentally injure someone.

We recommend taking private liability insurance with a coverage of at least 50 million euros. Moreover, ensure that your policy covers damages of at least 10 million euros per injured person.

Bad debt (Forderungsausfall)

Suppose someone caused damage to you. But they cannot cover it.

In this case, your private liability insurance covers the costs of the damages.

It’s like reverse liability insurance, where your own insurance covers the costs. Unfortunately, some insurers only cover damages up to 2,500 €.

So, carefully check the bad debt (Forderungsausfall) clause when comparing personal liability insurance.

15% of German households do not have third-party liability insurance. Thus, it is vital to have private liability insurance with bad debt coverage.

The Best Performance Guarantee (Die Best-Leistungsgarantie)

With the best performance guarantee, the insurer promises to act like the best insurer in the German market in case of a claim.

The best performance guarantee clause is handy when you cause damage, but your insurer refuses to cover it.

The reason could be that the tariff does not cover a certain area of life or that the compensation limit is insufficient.

But if you can prove that another insurance provider covers the damage, the benefits of the other insurer also apply to your liability insurance contract.

In short, the best performance guarantee clause raises insurance protection to the highest level available in Germany.

A tariff that includes a comprehensive best-performance guarantee is better than one that lists all the services but does not offer the best-performance guarantee or restricts it.

You can get personal liability insurance on comparison portals like Check24* and Verivox*. The personal liability insurance from “Die Haftpflichtkasse (Einfach Komplett)” is rated the best by all the rating agencies (Morgen & Morgen, Franke Bornberg, Stitftungs Warentest) and experts (Bierl, VMK, Finanztip).

The “best performance guarantee” has the following limitations.

- You can compare only German private liability insurance providers.

- You can compare insurers’ services at the same tariff level. For example, you cannot use the exclusive tariff of another insurer for comparison if you only have a basic tariff.

In short, the best performance guarantee includes the services that other German insurance providers offer in a comparable tariff.

Best performance guarantee according to the GDV model conditions

The German Insurance Association (GDV) recommends the minimum services every personal liability insurance policy should offer.

The liability insurance tariffs with “performance guarantee according to GDV model conditions” cover all the benefits GDV recommends.

Usually, tariffs with a “performance guarantee according to GDV” ensure a minimum level of liability protection, and you avoid the clauses in the small print.

Thus, ensure that you pick a policy that offers a performance guarantee according to GDV.

Deductible

Opting for a deductible can reduce your insurance premium. You can check how much you save on insurance contributions by varying the deductible on Check24* and Verivox*.

NOTE: The insurer has the right of contract termination once a claim has been settled.

If the insurer cancels the contract, you may have to pay higher contributions on future liability insurance tariffs. Thus, request your insurance company to allow you to cancel the contract instead.

Lost keys

If you lose the keys to your rented apartment or office, your private liability insurance covers the costs.

If you lose the keys along with a document showing your address, the cost to replace them can increase exponentially.

In this case, the locks of every apartment in your rental property must be changed. Thus, having personal liability insurance with a lost keys clause can save you much money.

Data exchange

Many personal liability insurance companies offer tariffs covering electronic data transmission damages. And it is worth taking one.

For example, you went out to take a print. You unknowingly inserted a pen drive containing malware. Hence damaging the shop’s computer.

In this situation, you are liable to pay damages.

Moreover, the data exchange clause covers damages in the following situations.

- Data protection violations at work.

- Damages by accidentally deleting the data.

- Damage claims due to transmission of confidential data.

Moreover, you should consider taking cyber security insurance on top of personal liability insurance if you are self-employed and deal with user/customer data.

The personal damage to yourself on the internet can be covered by

- your household insurance (Hausratversicherung in German)

- or the personal liability insurance of the person who caused the damage

Cover your family members under the same private liability insurance

One liability insurance per household is sufficient if you are married or in a civil partnership.

Until your children’s education ends, they are also insured under your family contract. Moreover, your children don’t necessarily have to live in the same household to be co-insured.

Children under seven are only insured if the clause “Persons incapable of committing a crime (deliktunfähige Personen)” is included in the tariff.

Unmarried couples should ensure the co-insured person is named in the insurance contract.

Benefits of changing private liability insurance regularly

Here are the reasons you should change your personal liability insurance every year.

- Insurance companies revise their tariffs every year. Currently, the revisions lead to additional services and an increased insured sum, making it attractive to change insurance policies regularly.

- Many insurance providers offer bonuses or discounts to new customers. Hence, reducing the yearly contribution amount.

How do you change your personal liability insurance in Germany?

Cancel the contract, keeping the notice period in mind.

To switch liability insurance contracts, you must cancel the old contract three months before the contract renewal date. You can then look for a new, inexpensive private liability insurance policy with good coverage.

If you took third-party liability insurance from Check24* and Verivox*, you can cancel the policy on their portal in a few clicks.

Cancel the contract immediately.

You can cancel the liability insurance policy immediately in two scenarios.

- Your insurer announces a price increase without improving the benefits.

- You took a tariff that you can cancel anytime.

NOTE: Before terminating your insurance policy, check for a new insurance provider beforehand so that there are no gaps in insurance coverage.

When do you need special liability insurance on top of private liability insurance?

Even if you took the best liability insurance, it doesn’t mean all risks are covered. There are some areas for which you must take out special liability insurance.

Pet Owner Liability Insurance

In six federal states of Germany, taking dog liability insurance is compulsory. Irrespective of that, dog owners should have dog liability insurance for two reasons.

- You are liable for all damages your dog causes.

- Your private liability insurance does not pay for damages caused by dogs.

Moreover, you can find dog liability insurance with good coverage for under 50€ a year.

You can check dog liability insurance tariffs on comparison portals like Check24* and Verivox*. You can also check Getsafe* and Feather*. Getsafe and Feather are insurance agents that offer services in English.

Similarly, horse owners should take out horse liability insurance to cover themselves if their horse injures someone.

Drones liability insurance

Check whether your personal liability insurance includes drone protection if you use a drone personally. Otherwise, expand your insurance policy accordingly.

If you use the drone commercially, you must take out special drone liability insurance.

Builder’s liability insurance

As a builder, you are responsible for what happens on the construction site.

Hence, you should take a builder’s liability insurance (Bauherrenhaftpflichtversicherung) to cover the damages related to people’s injuries or damage to objects on the construction site.

Home and landowners liability insurance (Haus- und Grundbesitzerhaftpflichtversicherung)

Homeowners’ liability insurance is also known as building liability insurance or property liability insurance.

It covers the costs of damage to people or property and financial losses.

For example, someone slipped when you didn’t clean the snow in front of your property. Homeowner liability insurance pays damage claims.

If you own an apartment in a multi-family house, your building’s homeowners’ association takes liability insurance for the entire building. Hence, you don’t have to take one separately.

You can find good homeowner’s liability insurance on Check24*

You can read more about different types of liability insurance in Germany in our guide.

Different types of liability insurance in Germany

- You need different types of liability insurance based on your situation.

- All car owners must have motor vehicle liability insurance.

- Some types of liability insurance are mandatory, but all are highly recommended.

FAQs

Is personal liability insurance mandatory in Germany?

No, personal liability insurance is not compulsory in Germany. However, it is highly recommended that you take one.

It can protect you from going bankrupt.

Where can I find the liability insurance policy in English?

Getsafe* and Feather* offer services in English. Getssafe and Feather are insurance agents.

You can get personal liability insurance on comparison portals like Check24* and Verivox*. The personal liability insurance from “Die Haftpflichtkasse (Einfach Komplett)” is rated the best by all the rating agencies (Morgen & Morgen, Franke Bornberg, Stitftungs Warentest) and experts (Bierl, VMK, Finanztip).

How can I pay less for my liability insurance policy?

Here are some tips to save money on your liability insurance coverage.

- Change your private liability insurance every year to save money.

- Compare personal liability insurance tariffs on comparison portals like Check24* and Verivox*.

- Add a deductible to reduce the insurance premium.

- Pay insurance premiums yearly instead of monthly.

- Include all your family members under the same policy.

- Deduct the insurance cost from your tax return.

What happens if repairing the damaged item isn’t possible?

Suppose you accidentally damaged someone’s object that can’t be repaired. In this case, your personal liability insurer pays the actual cash value of the object to the injured party.

To calculate actual cash value, the insurance company takes the object’s current value and subtracts its depreciation.

More topics

References

- https://www.verivox.de/privathaftpflicht/haftpflichtschaden-melden/

- https://www.bdp-wirtschaftsdienst.de/wp-content/uploads/2009/12/Schadenbeispiele-Privat-Haftpflicht.pdf

- https://www.gdv.de/gdv-en

- https://www.finanztip.de/haftpflichtversicherung/privathaftpflicht/

- https://germanpedia.com/liability-insurance-germany