Get clarity on the home loan calculation methods used by German banks. Gain insights into how banks in Germany calculate interest on the mortgage and optimize for the maximum loan amount or minimum monthly installment.

Key takeaways

- Getting a low mortgage interest rate is not enough. You must pay attention to how banks calculate the interest on the mortgage.

- Banks may calculate interest on the principal left or on the initial principal. Mortgage offers that calculate interest on principal left are cheaper. Such mortgage offers are cheaper even if the interest rates are higher than the ones that calculate interest on the initial principle.

- You should calculate the maximum mortgage you can get to set your home-buying budget.

- As a real estate investor, you should calculate the minimum monthly installment. Real estate investors prefer low monthly installments to achieve high positive cash flow.

Table of contents

You are planning to buy a house in Germany. You have found your dream house and are looking for a mortgage to finance the house.

When exploring mortgage options, you should keep an eye on how the banks calculate the mortgage interest.

Many banks use financial techniques to charge more interest over the mortgage tenure. On the surface, it looks like a great offer. But in reality, it’s not.

In this guide, you’ll learn those financial techniques to make an informed decision.

How do German banks calculate the mortgage interest?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The borrowing rate offered by various banks can be the same, but how banks calculate interest may vary.

How banks calculate the interest rate can significantly affect the effective interest rate.

For example, let’s assume the below situation.

| Mortgage amount | 100k € |

| Interest rate / borrowing rate | 1% |

| Monthly installment (Principal + Interest) | 1000 € (916 € + 84 €) |

So, as per the above table, you took a mortgage of 100k € at a 1% borrowing rate per annum. You chose a monthly installment of 1000 €, consisting of a principal (916 €) and interest (84 €).

Bank 1: Calculates the interest rate on the principal left.

As you repay the mortgage, the principal will reduce over time. Thus, if the bank calculates the interest on the principal left, the interest part of the monthly installment reduces with time.

Continuing with the above situation.

| Mortgage amount | 100k € |

| Monthly installment (Principal + Interest) | 1000 € (916 € + 84 €) |

| After 1 year | |

| Interest paid | 1% of 100k € = 1000 € approx. or 84 * 12 = 1000 € approx. |

| Principal repaid | 916 * 12 = 11,000 € approx. |

| Mortgage amount left | 100k – 11k = 89k € approx. |

| After 2 years | |

| Interest paid | 1% of 89k = 890 € approx. or 75 * 12 = 890 € approx. |

| Principal repaid | 925 * 12 = 11,110 € approx. |

| Mortgage amount left | 89k – 11,110 = 77,890 € approx. |

You can see in the table above the interest you have to pay is reduced with the principal.

The image above shows the repayment plan of the borrower. The total interest paid in this example is 4457 €.

Bank2: Calculates the interest on the issued loan. (Annuity loan)

Bank2 offers the same interest rate as Bank1. But, it calculates the interest on the issued loan (i.e., $100k) and not the principal left.

This means that the interest portion of the monthly installment will stay the same throughout the loan term (i.e., $84).

In this scenario, you’ll pay TWICE the interest you paid in the previous plan.

| Mortgage amount | 100k € |

| Monthly installment (Principal + Interest) | 1000 € (916 € + 84 €) |

| After 1 year | |

| Interest paid | 1% of 100k = 1000 € or 84 * 12 = 1000 € approx. |

| After 2 years | |

| Interest paid The interest portion of the installment is fixed and is not reduced with the principal. | 1% of 100k = 1000 € or 84 * 12 = 1000 € approx. |

As you can see in the table above, the interest portion of the installment is not changing over time.

The borrower will take approximately nine years (100k / (916*12)) to repay the mortgage. Thus, interest paid in 9 years will be (9*12*84 = 9072 €). It’s twice the interest paid to bank1.

Thus, always check how the bank is calculating the interest.

Interhyp – Mortgage brokers in Germany

- Offer support in finding the right mortgage product.

- Help you understand the process of buying a property in Germany.

- A mortgage broker can find mortgage options from several banks within minutes.

Dr. Klein – Mortgage brokers in Germany

- Offer support in finding the right mortgage product.

- Help you understand the process of buying a property in Germany.

- A mortgage broker can find mortgage options from several banks within minutes.

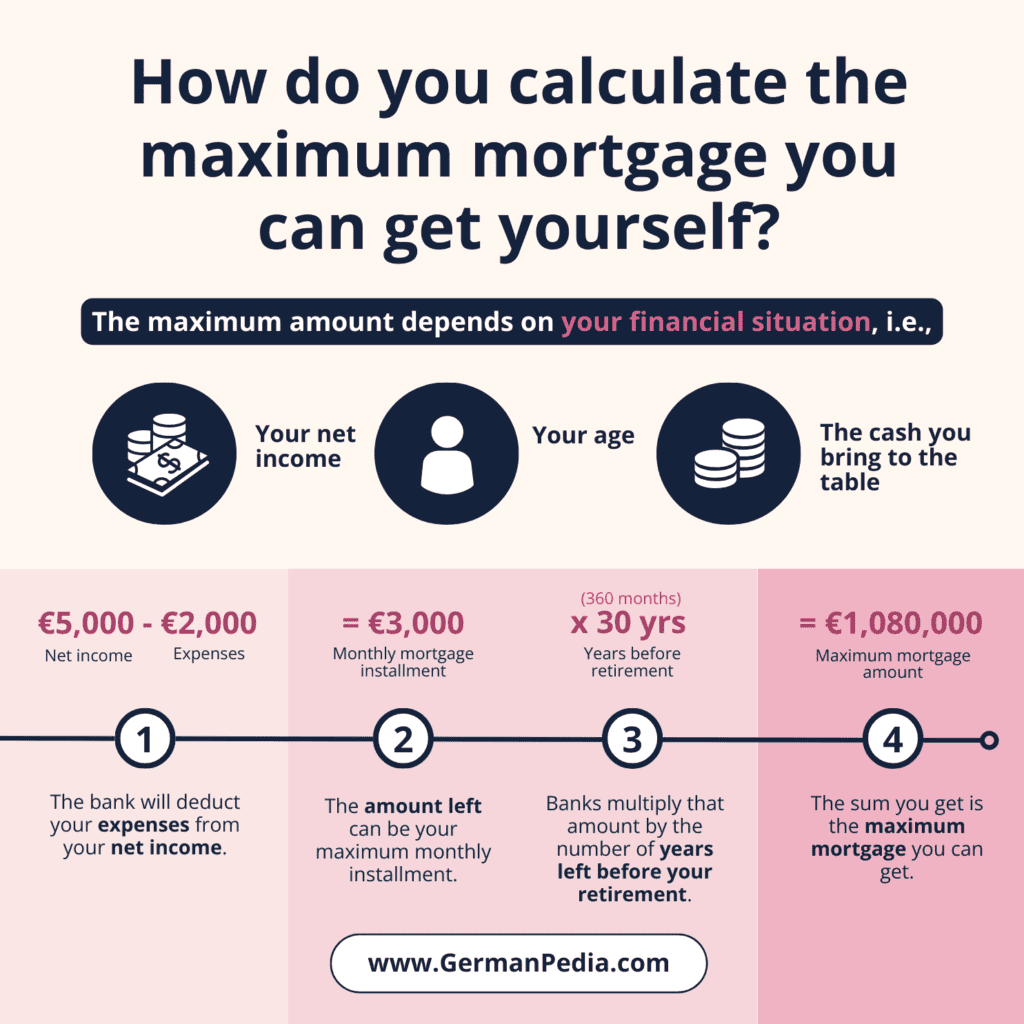

How do you calculate the maximum German mortgage you can get yourself?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The maximum amount of mortgage you can get depends on

- Your net income

- Your age

- The cash you bring to the table

Here are the steps banks follow to calculate the maximum mortgage amount.

- The bank will deduct your expenses from your net income.

- The amount left can be the maximum monthly installment you can pay.

- Lastly, banks multiply that amount by the number of years you can work until retirement.

- The sum you get is the maximum mortgage you can get.

For example:

| Age: | 30 Years |

| Household Income: | +4000 € |

| Living expenses* (without rent): | -2000 € |

| Other loans or monthly installments: | -500 € |

| Cold rent saved or received from the property: | +700 € |

| Operational expenses of the property: | -300 € |

| Maintenance of the property | -200 € |

| Maximum monthly installment: | 1700 € |

| Maximum mortgage you can get: | (Max monthly installment) * (Years of active employment) * Months in a year= 1700 * (65 – 30) * 12= 714k € |

* Generally, banks have a fixed amount they deduct based on the number of family members. They do not consider your actual expense.

As per this example, you have 1700 € left after deducting all the expenses. Thus, you can have a max of 1700 € monthly installment and borrow a max of 714k € loan.

NOTE: You have to bring at least “Nebenkosten” from your own pocket to be eligible for the mortgage. “Nebenkosten” is approximately 10% to 12% of the property’s purchase price.

So, if you want to borrow 700k € from the bank, you must bring at least 70k € to 84k € from your pocket.

How do you calculate the minimum monthly mortgage installment?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

You must be wondering why understanding the calculation of minimum monthly installment is important.

It’s because an investor wants to get the maximum positive cash flow from the property. That is the amount left after deducting all the expenses from the rent.

The low monthly installment helps the investor to achieve it. Thus, keeping the monthly installment as low as possible is vital for an investor.

In principle, banks want you to repay all the mortgage before retiring. Thus, check whether the minimum amount you want to repay every month aligns with it.

For example,

| Borrower’s age | 30 years |

| Retirement age in Germany | 65 years |

| Mortgage amount | 100k € |

| Mortgage interest rate | 2% |

| The minimum principal borrower has to pay to finish the loan before retiring. | (Mortgage amount) / (12 * (Retirement age – Borrower’s age) 100k / (12 * (65 – 30)) = 238 € approx. |

| Monthly installment | Monthly interest + Monthly principal ((2% of 100K) / 12) + 238 = 404 € approx. |

As per the table above, your minimum monthly installment to repay a mortgage of 100k€ is 404 €.

Even regular home buyers should consider low monthly installments to reduce the burden on their monthly expenses.

NOTE: The monthly principal and the total interest are inversely proportional to each other.

It means the higher the principal you repay, the lower the total interest you pay. Likewise, the lower the principal you repay, the higher the total interest you pay. Hence, find a balance between the two.

Master German Home Buying Process

in 12 Days For FREE

- Learn complete process of buying a house in Germany and how to invest in German real estate.

- Understand mortgage process, property documents and evaluation, and more.

- Expert tips that’ll save you thousands of euros.

- Know average renovation costs in Germany to plan and negotiate better.