Key Takeaways

- Legal protection insurance covers the legal expenses incurred in legal disputes.

- There are four major types of legal insurance in Germany: private life, work, residential housing, and traffic legal protection insurance.

- Legal insurance policy may cost from 70€ to more than 400€ per annum, depending on your personal situation and the legal services you choose.

- You cannot insure many areas of law in legal insurance.

- Legal insurance providers don’t cover legal disputes that existed before the contract was concluded or during the waiting period.

- You must take personal liability insurance and disability insurance before taking legal protection insurance.

This is how you do it

- Explore the alternative ways to resolve the dispute. If this doesn’t work, check whether legal protection insurance offers you the protection you seek.

- In our comparison and test, we found that KS-Auxilia*—Jurprivat, Arag*—Aktiv-Premium, and WGV—Optimal PBV are the best legal insurance plans.

- No legal insurance company in Germany offers services in English. There are insurance agents like Feather* and Getsafe* that can make the signup in English. However, the legal insurance policy they sell (Roland Insurance) offers services in German only.

- Check the insurance policy details to see whether the tariffs cover your desired legal services.

Table of Contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Need help communicating complex ideas visually? We help you turn data into your most persuasive story. Contact us to learn more.

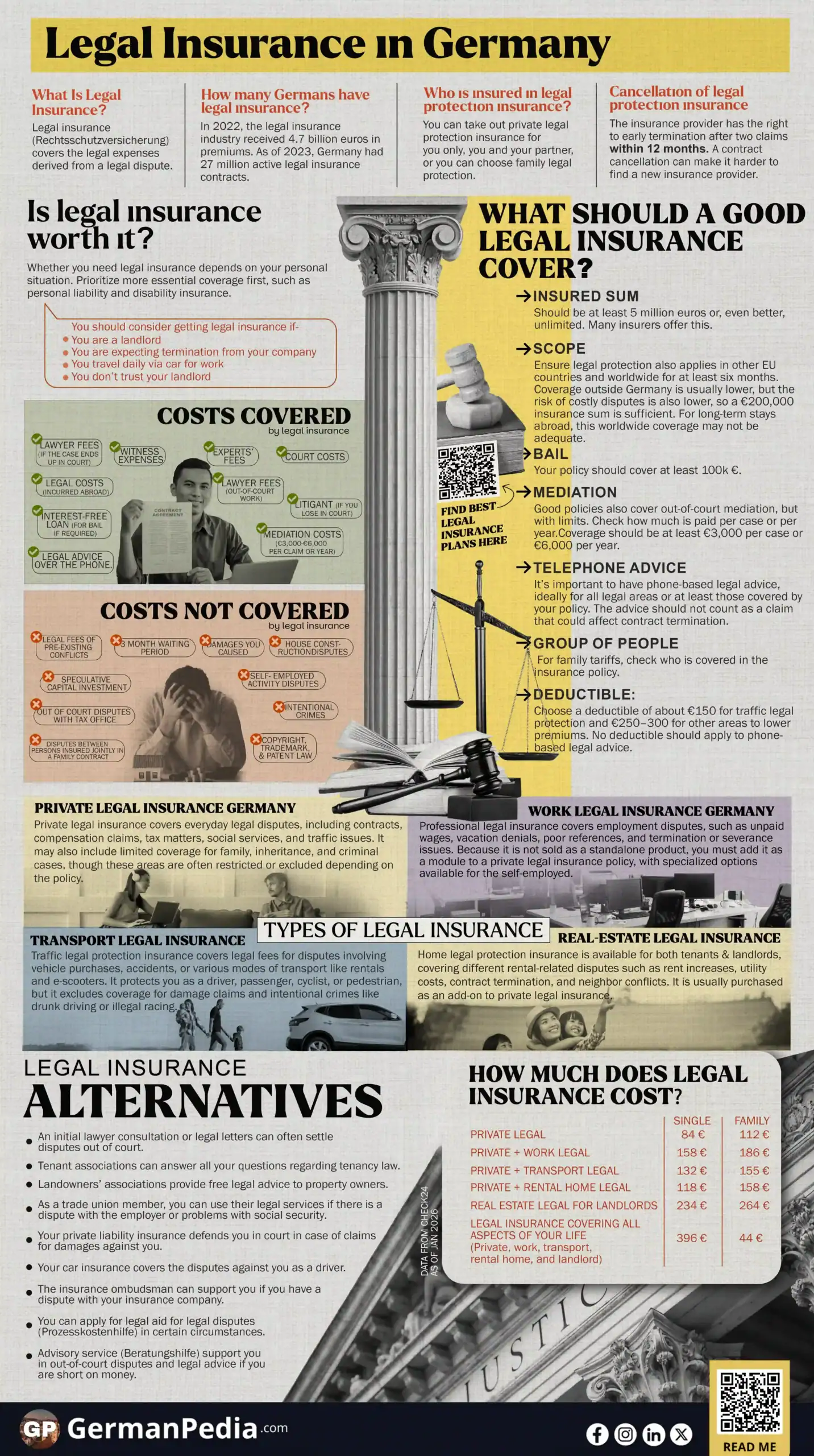

What Is Legal Insurance?

Legal insurance (Rechtsschutzversicherung in German) covers the legal expenses derived from a legal dispute.

How many Germans have legal insurance?

As of 2024, Germany had 27.3 million active legal insurance contracts. Moreover, four out of ten Germans would be willing to take legal action if the average cost of damage is around 600 €. [1, 2]

In 2022, the legal insurance industry received 4.7 billion euros in premiums and paid 3.2 billion euros in benefits to its customers. [2]

Is legal insurance worth it?

Whether you need legal insurance depends on two factors:

- Your personal situation.

- Probability of legal dispute.

However, you should first get insurances that are more important than legal insurance, such as personal liability insurance and disability insurance. If you don’t have liability insurance and seriously injure someone, it can be much more expensive than a legal dispute.

Let’s understand each factor in more detail.

Take legal insurance based on your personal situation

For example, traffic and employment legal insurance is worth it for someone who commutes to work by car daily and fears trouble at work.

On the other hand, a pensioner without a car doesn’t need any protection in these areas. Thus, assess your personal situation and accordingly consider taking legal insurance.

Probability of legal disputes

What is the risk that you’ll get into a legal dispute in the foreseeable future?

- Do you tend to push the speed limit, or do you always stay within limits?

- Is your workplace safe and your employer friendly?

- Do you have a good relationship with your neighbors?

- Do you think you can resolve disagreements without taking legal action?

The less likely you need a lawyer or even have to go to court, the less you need legal protection insurance.

Conclusion

- First, take important liability insurance policies

- Then check how often you expect to get into legal disputes

- Lastly, how much will the legal dispute cost you?

You should consider getting legal insurance in the following situations.

- You are a landlord

- You are expecting termination from your company

How should you behave when your employer terminates your contract? ->

- You travel daily via car for work

- You don’t trust your landlord

Learn your rights as a tenant in Germany ->

Best legal insurance in Germany

In our comparison and test, we found that KS-Auxilia*—Jurprivat, Arag*—Aktiv-Premium, and WGV—Optimal PBV are the best legal insurance plans.

Unfortunately, no legal insurance provider in Germany offers services in English. Insurance agents like Feather* and Getsafe* offer basic English support. However, when you need legal advice, you must contact the insurance company, which only offers advice in German.

Feather and Getsafe sell Roland’s legal insurance plans.

KS/Auxilia Legal Insurance

- Rated best legal insurance by the top rating agencies in Germany

- 15€ Amazon coupon

- Free legal consultation

- Offers comprehensive legal coverage

WGV Legal Insurance

- Rated best legal insurance by the top rating agencies in Germany

- Free legal consultation

- Offers comprehensive legal coverage

Arag Legal Insurance

- Rated best legal insurance by the top rating agencies in Germany

- The biggest legal insurance provider in Germany

- Free legal consultation

- Offers comprehensive legal coverage

Feather Legal Insurance

- Legal insurance policy starting from €13.51 per month

- Free legal consultation

- English customer support

- An insurance agent that sells Roland’s legal insurance policy

NOTE: Top rating agencies in Germany rated Arag—Aktiv-Premium, WGV—Optimal PBV, and KS / Auxilia—Jurprivat as the best legal insurance plans in Germany (as of Jan 2026).

NOTE: If you have special needs, consult an insurance broker to find the right legal insurance plan.

Legal insurance alternatives in Germany

- Get free legal advice to assess the legal costs and chances of winning the legal dispute. Based on the lawyer’s advice and legal expenses, you can decide whether pursuing a lawsuit is worth it.

How are legal costs calculated in Germany ->

- Hire a lawyer to settle the dispute out of court. This includes sending legal letters, a lawyer contacting the other party, etc. Hiring a lawyer to settle the dispute out of court is cheaper than taking the dispute to court. Moreover, many disputes can be settled out of court. You can find English-speaking lawyers here.

- Tenant associations (Mieterverein in German) can answer all your questions regarding tenancy law in Germany.

- The membership fee is 70 to 120 € per annum (depending on the city). It’s way cheaper than taking home rental legal insurance.

- As a member, you receive free advice on problems with the rental property.

- The Tenant Association also offers a lawyer to help members resolve disputes out of court.

- You receive legal support immediately after joining the association.

- Similarly, Landowners’ associations (Vermieterverein in German) provide free legal advice to property owners.

- As a trade union member (Betriebsrat), you can use their legal services if you have a dispute with your employer or issues with social security.

- Your private liability insurance defends you in court in case of claims for damages against you. Even if there is a lawsuit, you don’t have to pay anything for it.

- Your car insurance covers disputes against you as a driver. Initial legal advice on traffic law is often provided to members of automobile clubs such as ADAC. You need traffic legal insurance if you want to file a lawsuit against another driver.

Things your car insurance must cover ->

- The insurance ombudsman (Versicherungsombudsmann in German) can support you if you have a dispute with your insurance company. The insurance ombudsman tries to settle the dispute out of court. Hence, saving you court fees. Additionally, the insurance ombudsman’s services are free of charge.

- You can apply for legal aid for legal disputes (Prozesskostenhilfe in German) in certain circumstances.

- Advisory service (Beratungshilfe in German) supports you in out-of-court disputes and legal advice if you are short on money. You can obtain a counseling aid certificate (Beratungshilfeschein in German) from the local district court responsible for your place of residence.

Types of legal insurance in Germany

There are four common legal insurance types in Germany.

- Private life legal insurance (Privat-Rechtsschutz)

- Work legal insurance (Berufs-Rechtsschutz)

- Transport legal insurance (Verkehrs-Rechtsschutz)

- Real-estate legal insurance (Wohn-Rechtsschutz)

The advantage of dividing legal insurance into different categories is that you pay for the services you need. Thus, assess the areas important to you and take the legal insurance policies accordingly.

The table below shows the five most claimed categories in legal protection.

| Damage Category | Description |

|---|---|

| Contracts | Purchase contracts, rental contracts, travel contracts |

| Traffic | Fines, driving license withdrawal, hit and run, dangerous bodily harm |

| Damages | Damages and compensation for pain and suffering, accidents, dog bites, medical treatment errors |

| Work | Warning, dismissal, false testimony |

| Residential | Neighborhood disputes, rent increases, utility bills |

What can you do if your employer refuses to pay wages ->

#1 Private legal insurance Germany (Privatrechtsschutzversicherung)

Private legal insurance covers the following areas of your everyday life.

- Contracts – Covers you for legal disputes about travel, purchase, service, and insurance contracts. For example, a craftsman makes a mistake, and you want them to pay for it, or you demand a refund due to travel issues.

- Compensation – Supports you in claiming damages, such as after a car, bicycle, or foot accident.

What to do if you find yourself in a car accident outside Germany ->

- Tax – Legal dispute with the tax office. For example, legal disputes about the recognition of special expenses, income-related expenses, or extraordinary burdens.

- Social services – Legal insurance also covers the costs of legal disputes with German social services. For example, issues with your health insurance company, getting recognition for an occupational disease, etc.

- Traffic and Driving – Trouble related to traffic and driving authorities. For example, your driver’s license was revoked, and now the authorities refuse to issue it.

- Inheritance and family – Advice on adoption, child support, custody, or inheritance. Usually, legal insurance providers exclude this area. Ensure your insurance policy includes it if it’s important to you.

- Criminal law – The insurance cover applies to traffic, administrative, and negligent offenses. However, if the authorities accuse you of intentionally committing the crime, your legal insurance may not cover the legal costs. But if you are acquitted, the insurance company will reimburse the legal expenses.

Supplementary modules to cover legal costs

- Extended criminal legal protection – It covers you for criminal cases in which authorities accuse you of intentionally committing an offense. However, you must pay back the legal expenses if found guilty.

- Extended legal protection for the Internet – As the name suggests, this covers you in case you are a victim of cyber crimes. Many legal insurance policies offer this as an add-on.

#2 Work legal insurance Germany (Berufsrechtsschutz)

As we saw earlier, private legal insurance doesn’t include legal issues relating to your job. For this, you need professional legal insurance.

Unfortunately, no insurance provider offers professional legal insurance individually. Hence, you need to combine it with other types of legal insurance.

Normally, you buy work legal insurance as an additional module to the private legal insurance. There is special work legal protection insurance for the self-employed.

Here are some common situations where professional legal protection insurance can support you.

- Your employer is not paying the wages

- You don’t get any vacation

- You get a bad job reference

- Disputes about a warning, termination, or severance pay

#3 Residential legal insurance Germany (Wohnrechtsschutzversicherung)

Both tenants and landlords can purchase home legal protection insurance. Of course, the coverage differs between the two.

The tenant’s home legal insurance covers the following legal conflicts.

- Dispute over a rent increase

- Billing of ancillary costs

- Rental contract terminations due to personal use and eviction

- Dispute between neighbors.

The landlord’s home legal protection insurance covers the following conflicts.

- Rent increase

- Rent reductions or defaults

- Utility costs (Nebenkosten in German)

- Move out and security deposit

- Termination of the rental contract due to your (landlord’s) personal needs

- Disputes with the authorities, e.g., waste disposal fees

- Credit checks on a potential tenant can also be insured

Like work legal insurance, you cannot buy residential legal insurance individually.

In most cases, private legal insurance is the base insurance on which you can add other types of legal insurance. But there are insurance providers who offer other insurance policy combinations.

For example, ADAC offers traffic legal insurance as the base insurance on which you can add other types of legal insurance.

#4 Traffic legal insurance Germany (Verkehrsrechtsschutz)

You can purchase the traffic legal protection module individually or alongside private legal insurance.

Traffic legal insurance covers

- You and all the passengers.

- The insurance also covers you if you are driving someone else’s vehicle, e.g., a rental car or e-scooter.

- Legal dispute after buying a car

- Legal disputes after an accident if you were a pedestrian or cyclist.

- Some insurers even offer coverage for all “modes of transport.”

The insurance company pays the following legal fees if a dispute goes to court.

- Lawyer fees (your’s and opposing)

- Court fees

- Costs of an expert.

Traffic legal protection insurance doesn’t cover

- Defense against claims for damages. Your car insurance usually covers it.

- Intentional crimes, e.g., illegal car racing, coercion through tailgating, or drunk driving.

What should a good legal insurance cover?

A good legal insurance tariff should meet the following criteria.

- Insured sum: The insured sum should be at least 5 million euros or unlimited.

- Scope: Ensure the legal protection also applies in other EU countries and worldwide for at least six months. The sum insured outside Germany is usually lower. But the risk of getting into an (expensive) legal dispute is also lower. Thus, an insurance sum of 200k € is sufficient. If you are traveling abroad for a longer period, this worldwide protection is not enough.

- Bail: Your policy should cover at least 100k €.

- Mediation: Good insurance policies also cover out-of-court mediation. However, the insurer limits the maximum amount covered. Thus, check how much the insurance company pays per case or year for mediation. It should be at least 3,000 € per case or 6000 € per year.

- Telephone advice: It’s vital that you have the option to ask legal questions over the phone. Ideally, questions in any legal area. But at least for the areas you are insured. On top of it, it’s critical that the advice over the phone should not be considered a claim relevant to contract termination.

When can the legal insurance company cancel your contract in Germany? ->

- Group of people: For family tariffs, check who is covered in the insurance policy.

- Deductible: Choose a deductible of around 150€ for traffic legal protection insurance and 250€ to 300€ for others. Having a deductible reduces your yearly insurance contribution. No deductible should be due for legal advice over the phone.

NOTE: The insurance company can cancel the contract after two claims within twelve months. Thus, you should avoid reporting small cases.

| Criteria | Single | Family | Car Drivers |

|---|---|---|---|

| Total Insurance Sum | 5 million euros | 5 million euros | 500k euros |

| Insurance Sum Worldwide (Outside Germany) | 200k euros | 200k euros | 100k euros |

| Insurance Validity Period Outside Germany | at least 6 months | at least 6 months | at least 6 months |

| Bail amount | 100k euros | 100k euros | 100k euros |

| Deductible (Selbstbeteiligung) | 250 – 300 € | 250 – 300 € | 150 € |

| Extended Criminal Protection | Optional | Optional | – |

| Children insured | N.A. | Yes | Yes (N.A. for singles) |

| Partner insured | N.A. | Yes | Yes (N.A. for singles) |

| Mediation Costs | 3000 € per case or 6000 € per year | 3000 € per case or 6000 € per year | 3000 € per case or 6000 € per year |

| Telephone Consultation | Free consultation without contract termination | Free consultation without contract termination | Free consultation without contract termination |

Other things to consider while taking legal insurance

The criteria below are not relevant to everyone, but they are worth mentioning. Consider whether they are important to you.

Consecutive Event Theory (Folgeereignistheorie in German)

Legal protection insurers in Germany do not cover the cost of the disputes that began before you took out the insurance. Thus, it’s essential to understand how the insurance company judges the beginning of the dispute.

Legal insurers determine the start of the dispute in two ways.

- When the actual damage occurred, or

- When the event that caused the damage occurred.

For example, you buy a bicycle and take out legal insurance afterward. You had an accident a year later. The bike’s frame broke during the accident due to a material defect. You want to sue the person who caused the accident to claim damages.

In this case, depending on how your legal insurance provider determines the start of the dispute, the insurer may or may not cover the cost.

- Suppose your insurer doesn’t see the start of the legal dispute in the accident, but in purchasing the defective bicycle. Because you purchased legal insurance after buying the bicycle, the insurer won’t cover the legal costs.

- Suppose your insurer sees the start of the legal dispute in the accident. In this case, they cover the costs.

To avoid case 1, you should obtain a legal insurance policy with a consecutive events(Folgeereignistheorie) clause. Under this clause, the dispute begins when the damage occurred.

NOTE: An insurance policy with consecutive event theory clause can be expensive. So, if you don’t have very expensive items, the additional cost for the added protection might not be worthwhile.

However, an increasing number of tariffs now include protection under “consecutive event theory”. So, if it doesn’t cost much, you should add it to your insurance cover.

Extended criminal legal protection (Erweiterter Strafrechtsschutz in German)

Under this clause, legal insurance covers you even if you are accused of committing a crime intentionally. However, if you are found guilty, you must reimburse the insurer for the legal costs.

Extended criminal legal protection makes insurance expensive and reduces the number of tariff options. You should avoid it if the insurance becomes too costly for you.

Moreover, if it turns out you were wrongly accused, the insurance company will pay the costs of the legal dispute afterward anyway.

Who is insured in legal protection insurance?

You can take out private legal protection insurance for

- you only,

- you and your partner,

- or you can choose family legal protection. This insurance policy covers adults and unmarried children. The insurance also covers the children if they no longer live at home. But only until they get a job.

Many tariffs include other family members living in the household. For example, if your parents or parents-in-law live with you in the same household, you should consider taking a plan that also covers them.

What legal costs does legal insurance cover in Germany?

The legal insurance covers the following legal fees depending on your contract.

- court costs,

- witness expenses

- experts’ fees,

- costs of the litigant if you lose in court,

- legal costs incurred abroad (e.g., translation and travel costs),

- an interest-free loan for bail if required,

- lawyer fees if the case ends up in court,

- lawyer fees for out-of-court work,

- mediation costs – either in full or up to a maximum amount, depending on your tariff. The costs are usually between 3,000 and 6,000 euros per claim or year,

- getting legal advice over the phone. Many insurers offer a 24/7 hotline to get legal advice over the phone. You can even ask questions about areas your insurance policy doesn’t cover.

Note: You must inform your insurance company before entering into a legal dispute. Only with the confirmation of coverage can you be sure that your legal insurance company will pay.

What does legal insurance not cover?

Having legal protection insurance doesn’t mean you have unlimited coverage. There are several restrictions and situations that legal insurance doesn’t cover.

- The insurer doesn’t cover the legal fees of conflicts that exist before concluding the contract.

- You often have three months or longer waiting periods before you can claim insurance benefits. But there are exceptions. For example, there is no waiting time in the event of a traffic accident.

Legal insurance in Germany does not cover legal fees in the following cases.

- Legal insurance doesn’t pay your fines.

- Someone sues you for the damages you caused. In this case, you should have liability insurance.

- Disputes in the area of construction and construction financing of houses, apartments, etc. (e.g., “planning,” “construction or renovation of a property,” and “purchase or sale of a building plot”).

- Intentional crimes.

- Copyright, trademark, and patent law.

- Speculative capital investments, such as gaming and betting contracts.

- Legal trouble in connection with your self-employed or commercial activities. There is special legal insurance for commercial or self-employed people.

- Disputes between persons insured jointly in a family contract, such as spouses.

- Out-of-court disputes with the tax office or a social welfare office.

The cases excluded from insurance coverage vary by insurance provider.

Legal insurance policies rated the best by independent trading agencies in Germany ->

Litigation costs in Germany

Court costs in Germany depend on the amount in dispute. The amount in dispute is the maximum claim the winning party may get.

| Legal Cases | Amount in dispute (in euros) | Court costs(in euros) |

|---|---|---|

| Rent reduction due to mold | 4693 | 2259 |

| Landlord evicting you from the rental property for their personal use | 8940 | 3671 |

| Unfair job dismissal and bad job reference | 12300 | 4380 |

| Travel deficiencies on vacation | 2700 | 1554 |

| Revocation of a purchase contract for a defective new car | 37000 | 7405 |

Read our guide on how legal costs are calculated in Germany to learn more.

How much does legal insurance in Germany cost?

As you may guess, legal insurance costs depend on your personal situation, insurance plan, and the legal services you choose.

Here are the approximate costs of different types of legal insurance in Germany.

| Type of Legal Insurance | Average Cost per annum in euros (Single with 300 € deductible) | Average Cost per annum in euros (Family with 300 € deductible) |

|---|---|---|

| Private legal insurance | from 84 € | from 112 € |

| Private + Work legal insurance | from 158 € | from 186 € |

| Private + Transport legal insurance | from 132 € | from 155 € |

| Private + Rental home legal insurance | from 118 € | from 158 € |

| Real estate legal insurance for landlords | from 234 € | from 264 € |

| Legal insurance covering all aspects of your life (Private, work, transport, rental home, and landlord) | from 396 € | from 444 € |

NOTE: The insurance company assesses the risk of damage differently depending on where you live. Hence, legal insurance costs may vary depending on your place of residence.

You can also deduct the legal insurance premium from taxes. You can read more about it in our guide.

Cancellation of legal protection insurance in Germany

The insurance provider has the right to early termination after two claims within twelve months. However, legal advice over the phone should not count as a claim if the tariff is good.

Even if you rarely get into legal disputes, it can quickly lead to two claims.

For example, your employer gives you a termination notice. You want to defend yourself against this notice. But in the meantime, your employer issues you a bad job reference.

The German court considers the termination notice and bad job reference as two separate legal cases. In this case, the insurance company has the special right to terminate the contract.

A contract cancellation from your insurer can make it difficult for you to find a new insurance provider.

When applying to the new provider, you must answer questions about previous insurance. You must provide information on the number of claims in the last five years and who terminated the previous legal insurance policy.

NOTE: You should never give false information as it can endanger your insurance cover.

TIP: If your insurance provider gives you a contract cancellation notice, you should ask the insurer to withdraw the notice so that you can terminate the contract yourself.

Free Legal Insurance Cancellation Letter

- Download the legal insurance cancellation letter.

- You can use the letter as it is. You only need to fill in your details.

- The letter is available in both docx and pdf formats. Hence making it easy to modify.

What can you do if your legal insurance company doesn’t pay?

If your insurance company refuses to pay because it claims you caused the legal dispute willfully or that there is no chance of winning, you can appeal this decision.

You can appeal the insurer’s decision via an arbitrator’s report (Schiedsgutachten) or a casting vote (Stichentscheid).

The result of both procedures is binding for the insurer.

In the event of a dispute with your insurance provider, you can also contact an insurance ombudsman.

The insurance ombudsman examines the case free of charge and can oblige the insurance company to finance a lawsuit if it would not cost more than 10,000 €.

More topics