Key Takeaway

- Compare the car loan offers on comparison portals Verivox*, Finanzcheck*, and Check24*

- Do not accept the first offer you get. Calculate the total loan cost before you accept any offer.

- Never take a loan to satisfy your desires, especially for an item that loses its value with time.

- You can reject a loan offer without giving any reason. Moreover, you can also cancel a loan contract within 14 days without providing any reason.

Table of Contents

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Best car loan providers in Germany

You can find the best car loan conditions on one of the following comparison portals

Note: Comparison portals display the best interest rates and car loan conditions on their websites. But only after you apply for a car loan, you’ll get the actual loan conditions from the bank.

We recommend comparing the car loan interest rates and conditions on different portals before you sign the contract.

NOTE: You can compare as many offers as you want on comparison portals, but apply for the one that you find the best. Never apply for multiple offers on the same or different portals. It affects your Schufa score negatively.

Compare car loan offers on Verivox

- Top interest rates with around 40% savings

- Fast confirmation and payment

- Non-binding, free of charge and Schufa-neutral

Compare car loan offers on Finanzcheck

- 100% free

- Non-binding loan request

- 99.3% positive reviews

Compare car loan offers on Tarifcheck

- Free and without obligation

- Free advice from over 300 credit experts

- Guaranteed to be Schufa-neutral

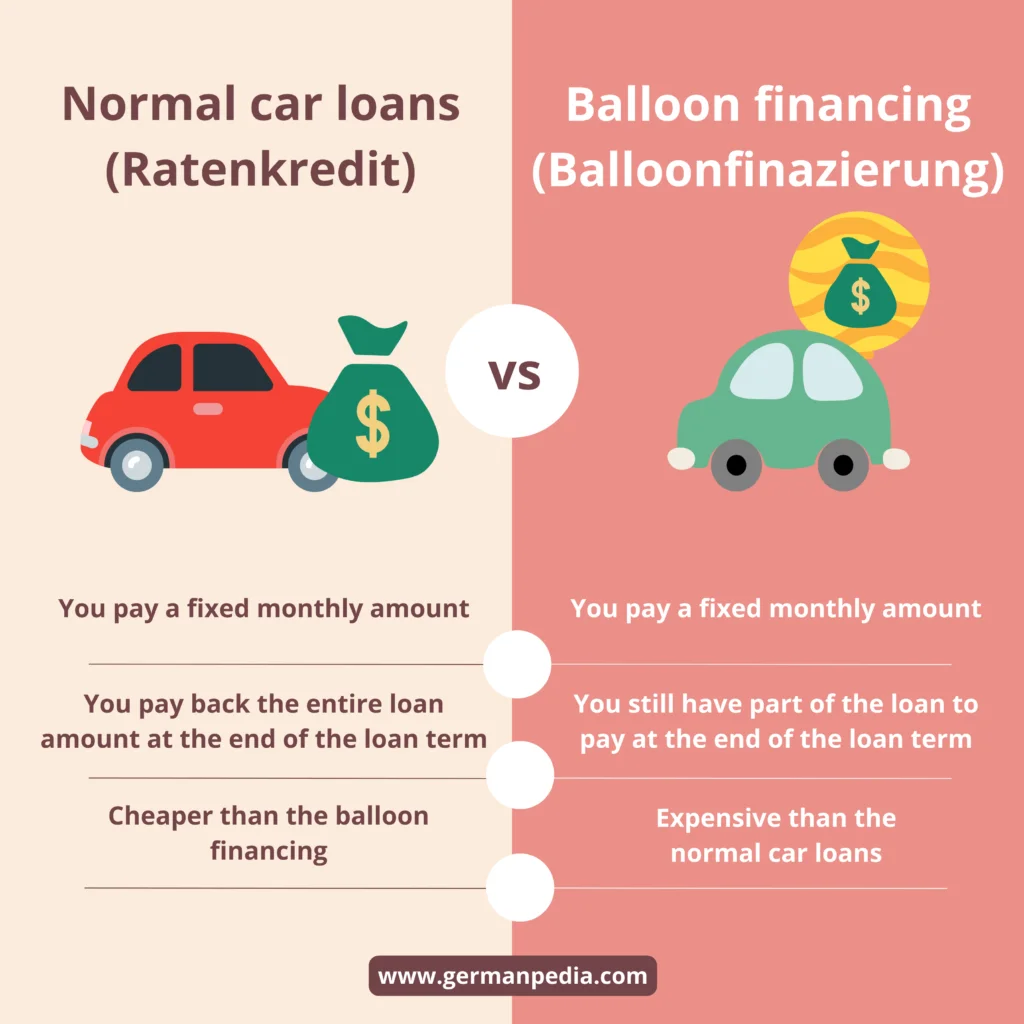

Different types of car loans in Germany

There are two types of car loans offered by different providers in Germany.

- Normal car loans (Ratenkredit)

- Balloon financing (Ballonfinanzierungen)

Normal car loans (Ratenkredit)

In this type of car financing, you pay a fixed monthly amount. You pay back the entire loan amount by the end of the loan term.

Such loans are cheaper than balloon financing.

Balloon financing (Balloonfinanzierung) or Three-way financing

In this type of car loan, you pay a fixed monthly amount. The monthly installment is lower than that of a normal car loan. At the end of the loan term, part of the car loan remains. The remaining loan amount is usually a big sum. Hence, known as “balloon amount” or “balloon financing”.

Car dealers often offer balloon financing, also called three-way financing. With balloon financing, the dealer offers three ways to repay the remaining loan amount.

- Purchase of the vehicle: You can buy the car at the end of the repayment period by paying the remaining balance (final payment/balloon payment).

- Returning the vehicle: You can return the car after the end of the financing period. However, you must fulfill the conditions, such as the number of kilometers driven, the car’s state, etc., set by the car dealers.

- Refinancing or follow-up financing: You can continue financing the vehicle. You must conclude a new loan agreement or extend the existing financing. In this case, new conditions and installment payments will be agreed upon to cover the remaining balance. Refinancing a car is usually expensive.

Comparison of loan costs in different types of loans

| | Normal car loan (in €) | Balloon financing (in €) |

|---|---|---|

| Car’s purchase price | 20,000 | 20,000 |

| Down payment | 5,000 | 5,000 |

| Loan amount | 15,000 | 15,000 |

| Loan Interest Rate | 6.3% | 6.3% |

| Loan term in months | 60 | 60 |

| Monthly rate/installment | 292.12 | 194.75 |

| Last installment | 292.12 | 5,000 |

| Total amount paid by you during the loan term | 17,527.2 | 18,564.90 |

| Total interest paid by you | 2,527.2 | 3,564.90 |

| Extra you paid in balloon financing | 1,037.7 |

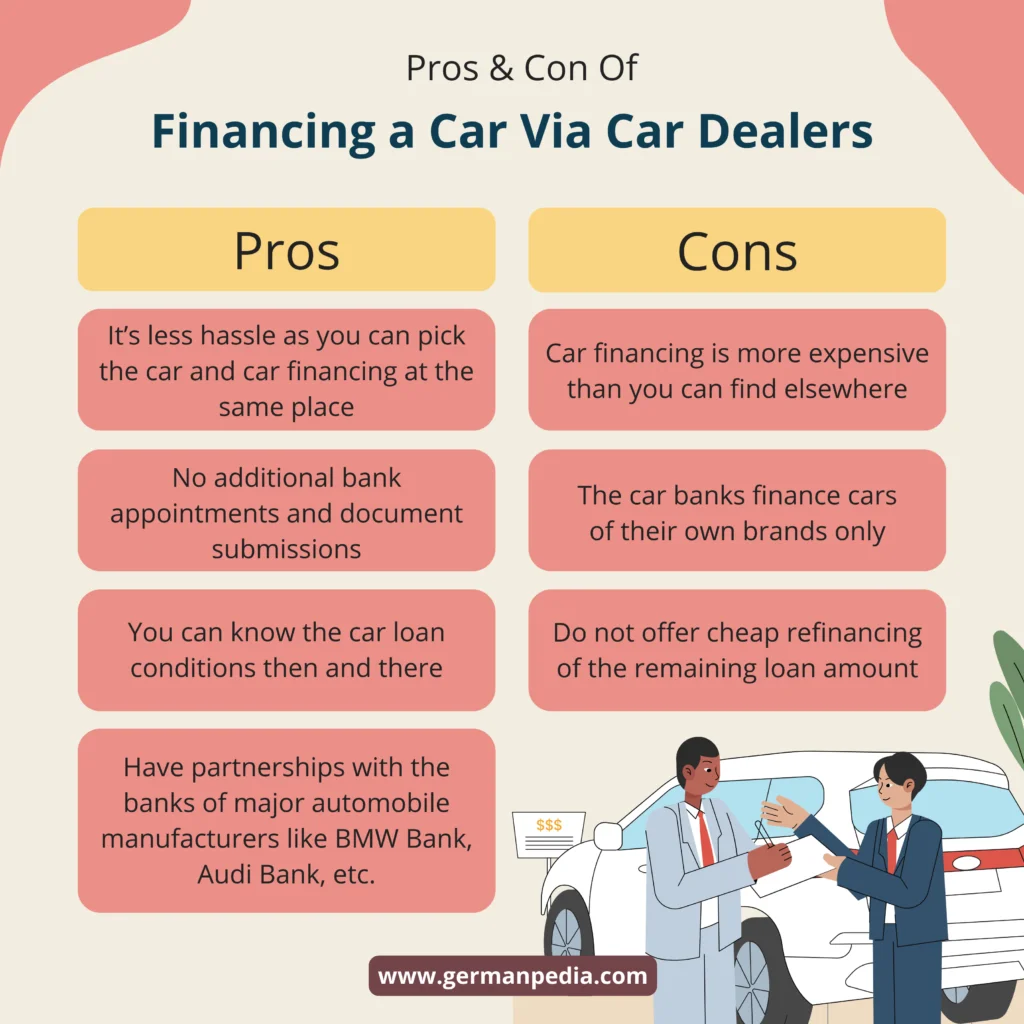

Financing a car via car dealers

Car dealers also offer car loans. But you shouldn’t accept the first offer you get.

You must compare different car financing offers on comparison portals like Verivox*, Finanzcheck*, and Check24* to find the best deal.

Advantages of financing a car via a car dealership

- It’s less of a hassle as you can pick up the car and get car financing at the same place.

- No additional bank appointments and document submissions.

- You can know the car loan conditions then and there.

- They have partnerships with the banks of major automobile manufacturers like Volkswagen Bank, BMW Bank, Audi Bank, and Mercedes Bank.

Disadvantages of financing a car via a car dealership

- Car financing via a car dealer is usually more expensive.

- Car banks finance cars of their own brands only. For example, Mercedes Bank offers car financing for Mercedes-Benz only.

- Some dealers offer special interest rates (e.g., 0% financing). However, you must ensure that they don’t inflate the car’s price or bundle it with additional products.

- Car dealers don’t offer cheap refinancing of the remaining loan amount.

How to apply for a car loan?

- Go to one of the comparison portals: Check24*, Verivox*, and Finanzcheck*.

- Enter the loan amount and loan term you wish for. You can make the amount higher than the actual purchase price to account for additional costs (E.g., registration fees, insurance). However, ensure that this amount is not too far from your car’s price.

- Enter your personal details or log in to automatically fill in the details.

- Enter your job and family details.

- Provide your monthly net income and expenses.

TIP: Fill in all the information requested by the comparison portal, including optional, to process things faster.

- Enter the car details that you want to buy. Choosing hybrid or electric cars may give you lower interest rates from some banks.

- Check what type of insurance you want. We recommend not taking any insurance as part of the car loan.

- Enter the bank account where you want to get the money.

Best bank accounts in Germany ->

Based on the above information, comparison portals will show offers from different banks. You can apply for the car loan offer you like directly on the comparison portal.

NOTE: You can compare as many offers as you want on comparison portals, but apply for the one that you find the best. Never apply for multiple offers on the same or different portals. It affects your Schufa score negatively.

Two more steps to complete the car loan application.

- Verify your identity. There are two options to verify your identity.

- Video call with a customer advisor. It is a faster and hassle-free option.

- At the post office: You go to a post office of your choice with your documents. A postal employee will confirm your identity on-site and forward your information to the bank.

- Last but not least, upload the documents requested by the bank. Banks usually process the application within 2 to 3 days.

If the bank accepts your application, it’ll send you a contract. Sign the contract and send it back.

Note: You can accept or reject the car loan offers without providing any reason. Moreover, you can cancel the car loan within 14 days of signing the contract without providing any reason.

Checklist for loan documents

- Download the checklist summarizing all the information and documents you need when applying for a loan in Germany.

- Maximize your chances of getting a loan in Germany.

- Submit the required information and documents to speed up the loan approval process.

What do you need to finance a car in Germany?

You need the following documents to apply for a car loan.

- You must be at least 18 years old.

- Personal identity document. It could be your passport, residency card, etc.

- Proof of income:

- For employees: last 3 months’ payslips and a work contract.

- For self-employed: recent tax statements or income verification documents.

Once you buy the car, you must also submit proof of car purchase or a vehicle registration certificate. The document you must provide depends on your car loan’s terms and conditions.

How to buy a car in Germany ->

Best car insurance in Germany ->

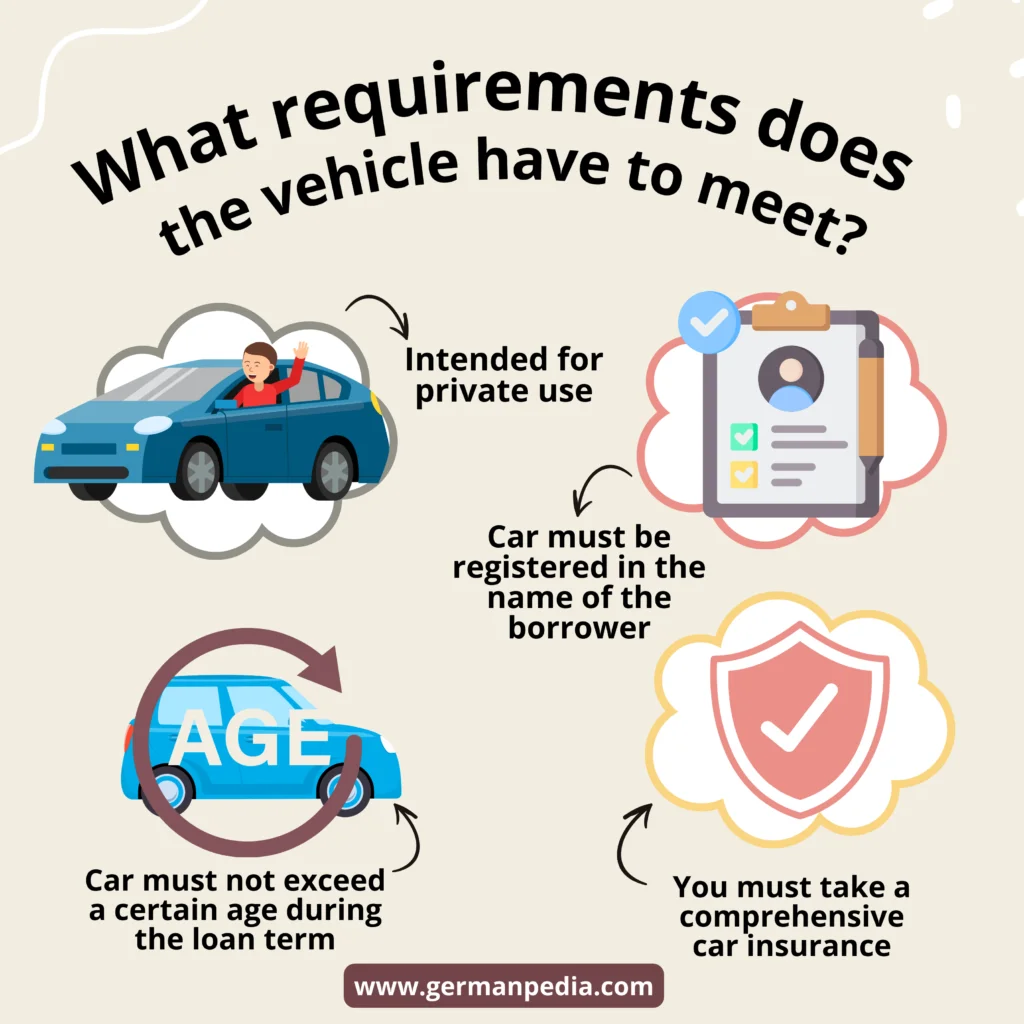

Financing a car — what requirements does the vehicle have to meet?

You can finance any car if you meet the bank’s creditworthiness requirements. However, banks also have certain requirements for the vehicle to be financed.

- The car must be intended for private use

- The car must be registered in the name of the borrower

- The car must not exceed a certain age during the loan term.

- The car must not exceed the set mileage during the financing period.

- The car must have a certain value (e.g., loan amount percentage)

- You must take comprehensive car insurance

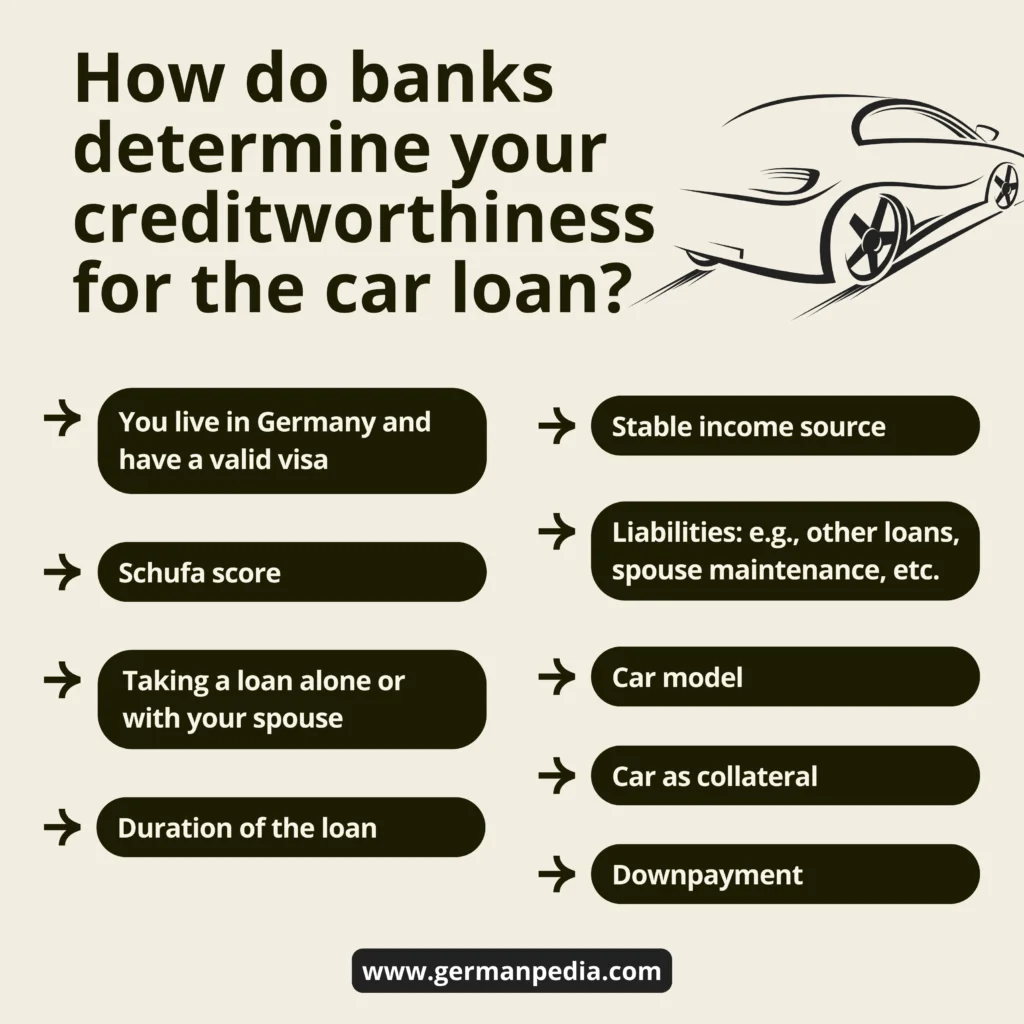

How do banks determine your creditworthiness for a car loan?

Banks calculate your creditworthiness to provide you with a binding car loan offer. The method to calculate it is different for every bank.

In general, banks consider the following aspects.

- Age: You are of legal age, i.e., 18 years.

- You live in Germany and have a valid visa or residence permit. Car loan interest rates offered to Bluecard holders are often higher than those provided to permanent residents or citizens.

- Stable income source: People with permanent job contracts get better car loan conditions than people with fixed-term contracts.

- Schufa score: Check for any incorrect Schufa entries that may negatively affect your Schufa score.

- Liabilities: e.g., other loans, spouse maintenance, etc. The fewer liabilities, the better car financing conditions you can expect.

- Taking a loan alone or with your spouse: Car loan conditions are usually better if you take a car loan with your partner. The reason is that the bank’s risk in this situation is spread out among two individuals.

- Car model: Banks also consider the car model when issuing car loans. Some banks offer better conditions for hybrid or electric cars.

- Car as collateral: Putting the car as collateral might fetch you better interest rates. Again, the risk for the bank in this situation is lower as the bank can recover the loan by selling the car.

- Down payment: Interest rate varies based on the amount of the loan you apply for and the car’s value. The higher the down payment, the better the car loan conditions you may expect. E.g., interest rates are higher for 100% financing than 80% financing.

- Duration of the loan: Interest rates increase with the increase in the financing period.

In short, the lower the risk for the bank, the better car loan conditions you’ll get.

How much does a car loan cost?

The cost of a car loan depends on the loan interest rate and the loan term. You can see the total loan costs for different terms and conditions in the table below:

| Loan amount | Loan term | Interest rate | Monthly rate | Total cost |

|---|---|---|---|---|

| 10,000 | 48 months | 6.3% | 236.25 | 11,340 |

| 10,000 | 60 months | 6.3% | 194.75 | 11,685 |

| 10,000 | 72 months | 6.3% | 167.17 | 12,036 |

| 10,000 | 48 months | 2.26% | 218.12 | 10,469 |

| 10,000 | 60 months | 2.26% | 176.45 | 10,587 |

| 10,000 | 72 months | 2.26% | 148.68 | 10,704 |

As you can see in the above table, the faster you repay the loan, the less interest you pay. Hence, try to repay the credit as soon as possible. Especially when the interest rates are high.

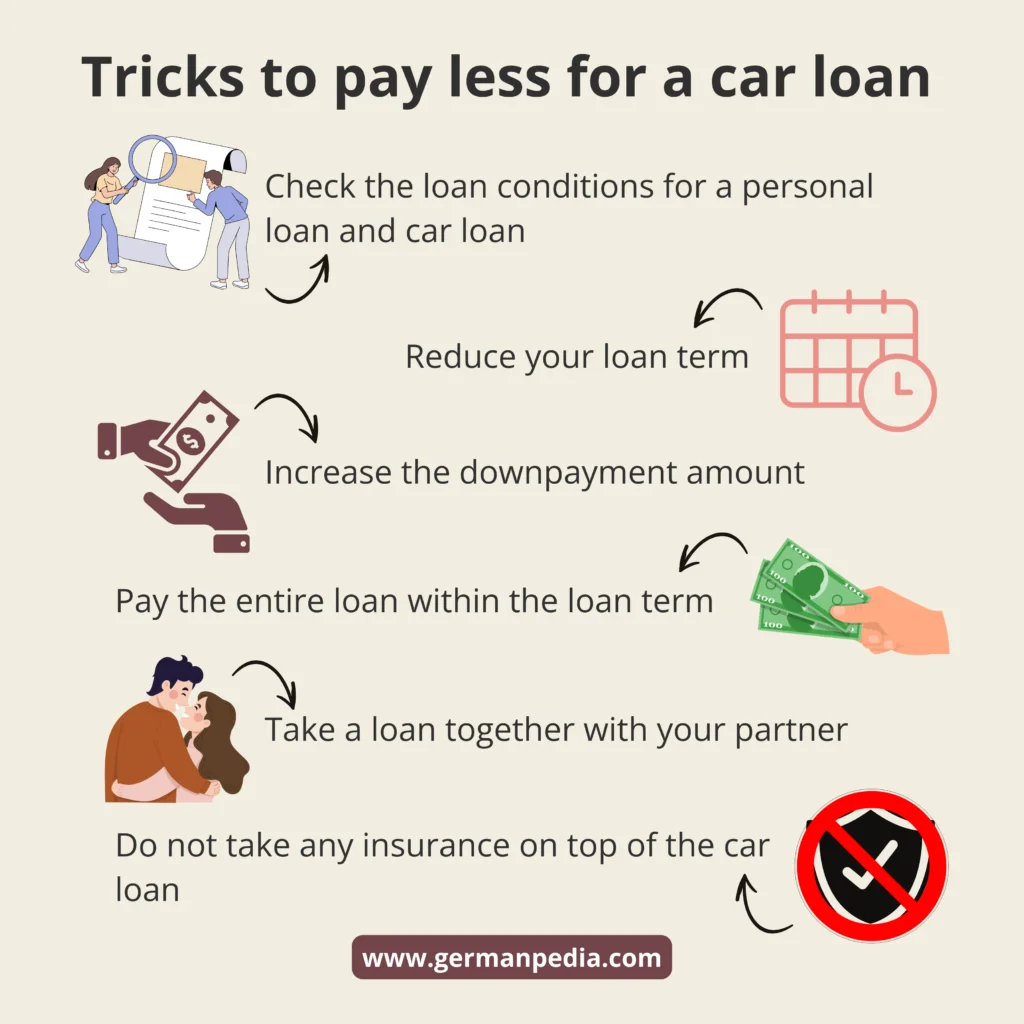

Tricks to pay less for a car loan

Here are some ways you can get a cheaper car loan.

- Some banks offer better conditions for personal loans than for car loans. Hence, also check personal loan offers. Compare the loan offers on comparison portals: Verivox*, Finanzcheck*, and Check24*.

- Reduce your loan term. The faster you pay back the loan, the cheaper it will be.

- Increase the down payment amount.

- Pay the entire loan within the loan term.

- Take a loan together with your partner.

- Do not take any insurance on top of the car loan. You don’t need residual debt insurance. It’s not worth it.

- Get the special repayment option. With this option, you can pay an additional amount on top of your monthly installments to repay the loan. As you repay the loan early, you pay less interest overall.

- Check the interest calculation method carefully.

Learn more about different interest calculations used by German banks ->

We recommend experimenting with the different options and checking which combination yields the best car financing offer.

Never take any insurance on top of the car loan

Almost every bank in Germany offers residual debt insurance (Restschuldversicherung in German) while offering a car loan.

Residual debt insurance pays the car loan if you die or become unemployed. Such insurance is usually expensive and unnecessary.

Banks add the monthly insurance premium to the car loan installments. Hence, making the car loan expensive.

Instead, take unemployment and life insurance separately. Everyone should have term life insurance to protect their family’s financial well-being when they are gone.

You can use our term life insurance calculator to calculate the insured sum.

Term Life Insurance Calculator

- Calculate the amount you must insure to protect your loved ones.

- The calculator calculates the amount based on three methods.

- Years-Until-Retirement method

- Standard-of-Living method

- Debt, Income, Mortgage, Education (DIME) method

When does it make sense to take a car loan?

In general, we never recommend buying a car on loan. However, there could be situations where it may make sense to finance a car.

NOTE: Never take a loan to fulfill your desires. Especially for an item that loses its value over time, like cars

Need

You need a car and don’t have enough money to buy it. Then, taking a loan might make sense.

Still, you should explore all the options before you buy a car on loan, like public transport, car share, e-bikes, etc.

Cheap money

Taking a loan can be beneficial if the interest rates are lower than the inflation. However, you must then invest your own money to build assets.

Depending on your investment, you may earn more money over the loan term than the loan costs.

Things you should know after taking out a car loan in Germany

- You have a 14-day right to withdraw from a car loan. The bank must inform you of this in the loan agreement. If you no longer need the car loan for any reason, you can cancel the agreement within this period without providing any reason.

- Pay off the car loan early. You have the right to repay your car loan early. Banks may charge a prepayment penalty. However, the penalty is capped at 1% if the loan has more than twelve months remaining, and at 0.5% for shorter terms. Some banks waive this penalty entirely.

- Some car loan agreements contain mistakes, especially in the 14-day right to withdraw. In these cases, your right to withdraw stays valid indefinitely. If the dealer arranged the loan, it counts as a linked transaction. This allows you to cancel the loan even after 14 days and undo the car purchase.

- Contact your bank if you can no longer afford the monthly installments. If you stop paying your loan, you go into default. The bank can charge late fees, send reminders, and may eventually terminate the loan. This would require you to repay the full remaining amount at once. To avoid this, contact your bank as soon as you face payment issues. You can request a payment deferral, refinancing, or selling the car.

Frequently asked questions about financing a car in Germany

Yes, most lenders finance used cars. However, the car must meet their criteria (e.g., age limit, mileage limit, minimum value).

Yes, foreigners can get a car loan in Germany. But you must fulfill the requirements, such as

– valid resident permit (blue card or permanent-residence permit)

– stable source of income in Germany

– good creditworthiness

Yes, you need to provide the vehicle registration to the bank. The reason is that banks require the car as collateral or need proof of car purchase. Vehicle registration is the proof.

If the bank holds the vehicle as collateral, you cannot sell the car without the bank’s permission.

Yes, a car loan is generally a better option than a personal loan. The reason is that the bank can hold your car as collateral. This reduces the bank’s risk.

Suppose your bank holds the car as security against the car loan. In this case, you must submit the vehicle registration document (Zulassungsbescheinigung Teil II) to the bank.

Hence, making the bank the car’s legal owner during the financing period. Thus, you cannot sell the car without the bank’s consent during the car loan period.

Some banks only need proof of the car purchase. In this case, you are the car’s legal owner and can sell it anytime you wish.

However, if you don’t submit the car purchase proof, the bank may charge a higher interest rate on the car loan.

As per German law, banks must publish the maximum effective annual interest rate they charge to 2 out of 3 customers.

For example, a 2/3 interest rate of 6% means that the bank issued two out of three loans at an interest rate of 6% or less.

This information is useful as most of the banks and comparison portals show the best interest rates available. However, very few people get loans at such attractive interest rates.

0% financing lets you buy a car with no interest, paying only the purchase price in fixed monthly installments. These deals are rare and usually limited to promotional vehicles.

If you take a car loan with 0% financing, make sure to compare the vehicle’s total price on comparison portals and check for any unnecessary hidden costs.

No, you cannot deduct the interest from taxes for the loan you took for personal reasons. So, a car loan that you take out primarily for personal use cannot be deducted from your taxes.

However, you can use a commuter’s allowance to reduce your tax burden.

More topics