Key takeaways

- Your vehicle insurance coverage sum should be at least 50 million euros.

- There are several ways to save on car insurance in Germany.

- Change your auto insurance every year to reduce car insurance costs.

- Switch to an annual plan to save money.

- Car insurance cost depends on factors such as age, driving experience, SF-Class, car type, and city.

- Every vehicle in Germany should have at least third-party liability insurance.

This is how you do it

- The following car insurance plans are rated the best by Germany's top rating agencies and insurance experts: CosmosDirekt (Comfort)*, HUK24 (Classic with Kaskoplus), AXA (Comfort)*, Allianz (Comfort, Premium), and DEVK (Komfort-Schutz)

- You can compare car insurance plans on comparison portals like Verivox* and Check24*.

Table of contents

We recommend looking for new car insurance policies yearly as you may find a better and cheaper tariff.

Most car insurance companies have a deadline of November 30th to cancel the contract. So, look for a new one before this date.

Best car insurance in Germany

The following car insurance plans are rated the best by Germany’s top rating agencies and insurance experts.

- CosmosDirekt (Comfort)*

- HUK24 (Classic with Kaskoplus)

- AXA (Comfort)*

- Allianz (Comfort, Premium)

- DEVK (Komfort-Schutz)

CosmosDirekt car insurance

- Rated the best by rating agencies and insurance experts

- Offer competitive price

- Check which type of car insurance fit your needs (Third-party, Teilkasko, or Vollkasko)

Axa car insurance

- Rated the best by rating agencies and insurance experts

- Offer competitive price

- Check which type of car insurance fit your needs (Third-party, Teilkasko, or Vollkasko)

Tarifcheck – Compare car insurance plans

- Compare offers and prices.

- Comparison calculator to find the best car insurance in Germany.

- Compare the insurance providers and their ratings.

Verivox – Compare car insurance plans

- Compare offers and prices.

- Comparison calculator to find the best car insurance in Germany.

- Compare the insurance providers and their ratings.

Here is how we found the best car insurance plans

- First, we checked the top-rated car insurance plans by the rating agency Franke Bornberg. You can find their complete report here.

- Then, we checked the top-rated car insurance plans by Stiftung Warentest and the recommendations from insurance experts and blogs like Finanztip, TransparentBeratung, etc. This helped us narrow down the car insurance plans from 43 to 12.

- The next step was to check the customer reviews. Thus, we considered the customer satisfaction rating by DISQ. We also looked into customer complaints against car insurance companies. For this, we referred to the complaint data compiled by BaFin.

- Lastly, we scored all 12 car insurance plans based on customer satisfaction and the services offered to find the best car insurance in Germany.

What is car insurance in Germany?

Car insurance covers the costs of damage you cause to a third party while driving. Every car owner in Germany is legally required to have car insurance.

NOTE: Don’t confuse car insurance with personal liability insurance. Personal liability insurance doesn’t cover the costs of damage you cause while driving.

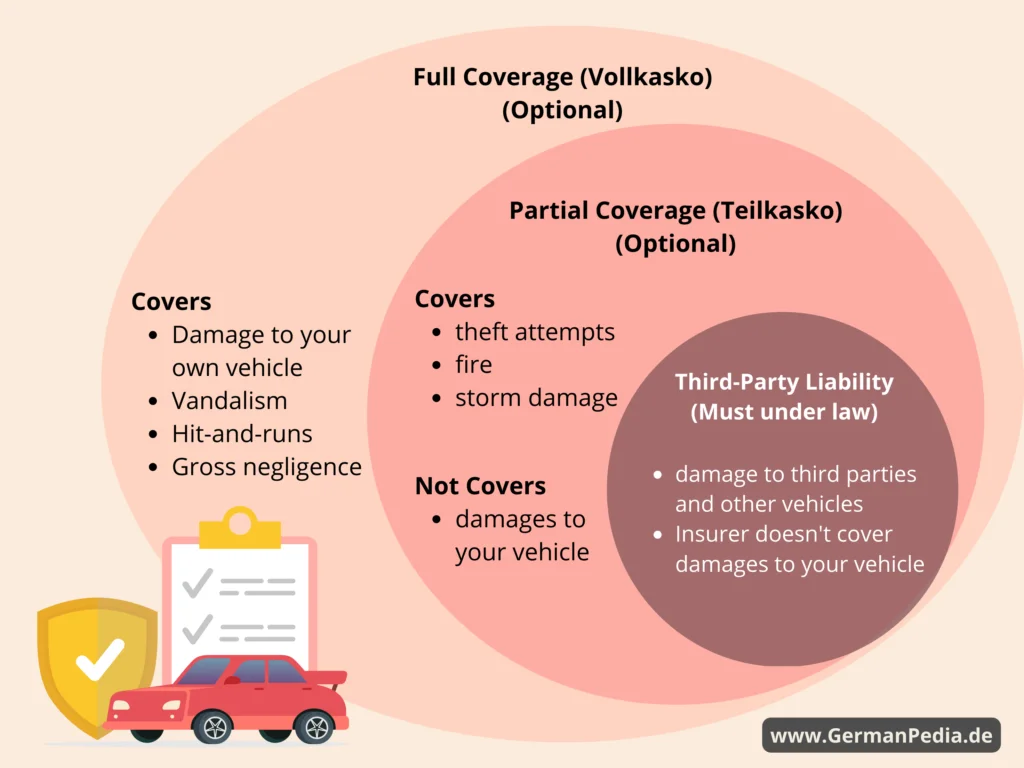

Types of car insurance in Germany

There are three types of car insurance in Germany.

- Third-party liability insurance (haftpflicht): Under it, the insurance provider covers the damage to third parties and other vehicles in the event of an accident. But the insurer doesn’t cover repair costs or damage to your car if you are responsible for the accident.

- Partial comprehensive car insurance (teilkasko): It covers third-party liability plus damages to your vehicle in some instances—for example, theft attempts, fire, storm damage, etc. It doesn’t cover damages to your vehicle if you caused the accident. The coverage benefits may vary depending on the car insurance.

- Full comprehensive car insurance (vollkasko): As the name suggests, it covers everything, including damage to your vehicle. In full coverage, it doesn’t matter if the accident is your fault. The insurer covers all the costs.

Partial and full-comprehensive car insurance costs significantly more than third-party liability insurance. So think carefully about whether you need this additional protection or not.

Which type of car insurance policy do you need?

Here is how you can decide which type of car insurance fits your needs.

- Full comprehensive coverage (Vollkasko)

- New cars

- Expensive cars

- You live in an area with a high probability of hit-and-run (e.g.: Berlin).

- Partial insurance coverage (Teilkasko)

- Expensive old cars

- Third-party liability insurance (haftpflicht)

- Cars older than 8 years

- Low-value cars. If the worst happens, it’s cheaper to replace the car

How do you find the cheapest vehicle insurance in Germany?

You have two options.

- Compare car insurance plans on comparison portals Verivox* and Check24*.

- Check the websites of car insurance providers. Sometimes, getting an offer directly from the insurance company can save you money.

The price of good auto insurance varies greatly. And no car insurance comparison portal displays all the insurance companies’ tariffs.

That’s why we recommend comparing the contracts on multiple portals, i.e., Verivox and Check24. The portals will give you a good overview of car insurance prices and conditions.

The following car insurance plans are rated the best by Germany’s top rating agencies and insurance experts.

- CosmosDirekt (Comfort)*

- HUK24 (Classic with Kaskoplus)

- AXA (Comfort)*

- Allianz (Comfort, Premium)

- DEVK (Komfort-Schutz)

What documents do you need to get car insurance in Germany?

- Personal identification documents, such as passport, residence permit, etc.

- German driving license

- Proof of the number of claim-free years if transferring no-claim years from your home country.

- Bank details if you choose SEPA direct debit. This way, the insurer can deduct the insurance premium automatically from your bank account.

- Vehicle purchase documents

How much does car insurance in Germany cost?

Car insurance in Germany costs between 100 € and 1000 € per annum. The wide range in car insurance costs is due to the fact that the cost depends on several factors.

- Car model or type class (Typeklasse): Statistically, some car models are involved in more accidents than others. So, car insurance companies charge higher premiums for such models. Audi S4 has had the most accidents in 2023 [1].

- City you live in or regional class (Regionalklasse): Some regions in Germany have more cases of thefts, accidents, etc. Living in a city with high theft or accidents means you’ll pay more car insurance premiums. One in three cars is stolen in Berlin. So, car insurance in Berlin is more expensive than in Stuttgart.

- SF class or number of accident-free or no-claim years: Car insurance companies give you discounts based on your SF class. The higher the SF class, the more discount you get.

- Insurance type: Third-party liability insurance is the cheapest, and fully comprehensive car insurance (Vollkasko) is the most expensive.

- Driver’s age: Drivers with more driving experience usually have higher SF Class. Thus, get higher discounts on car insurance premiums.

- Number of drivers: When you take car insurance, you mention how many drivers will drive the car. The more drivers you add, the more expensive the insurance gets.

- Vehicle’s value: Expensive vehicles have higher repair costs and value (if stolen), so the insurance premium is also high.

- Deductible: Deductible is the amount you pay on your own when a claim is made. The higher the deductible, the lower the car insurance cost. However, a deductible that is too high isn’t worth the amount you save on insurance costs.

- How will you use your car: Private or business? You pay more car insurance premiums if you use the car for business purposes.

- The number of kilometers you will drive. When you take out car insurance, you enter the number of kilometers you drive each year. The more kilometers you drive, the more risk of an accident. Thus, you pay a higher premium if you drive the car often.

How can you save on vehicle insurance in Germany?

- Opt for a “Deductible”: According to Finanztip’s analysis, a deductible of just 300 euros can save you up to 28 percent in car insurance costs.

- Switch to an annual payment plan: You can save up to 10% by switching from a monthly to an annual payment plan.

- Limit the number of drivers: The car insurance cost increases with the number of drivers you insure. So, keep the drivers to a minimum.

- Estimate annual mileage defensively: On average, car insurance costs increase between 8% and 15% every 5000 km.

- Let go of the option of picking a car workshop. You can save up to 11% by repairing your car at the workshop your insurer recommends.

- Car insurance for vehicles with seasonal plates is cheaper than those with normal license plates.

- Bring no claim bonus from your home country

- Change your car insurance every year. With each passing accident-free and no-claim year, your SF-Class is increasing. Higher SF Class fetches you higher discounts. Additionally, insurance companies offer discounts to attract new customers. Thus, changing car insurance every year can save you a couple of hundred euros.

How do you save on car insurance as a new driver in Germany?

- Ask your parents to insure the car in their name and add you as a second driver. This way, your parents’ SF Class is considered instead of yours. Hence, bringing the car insurance cost down.

- Take accident-free driving years from your parents’ car insurance contract to your new contract.

- Take the insurance from your family’s car insurance company.

- Gain driving experience with an accompanying driver. In Germany, you can get a driving license at the age of 17. The prerequisite is that an experienced driver should always accompany you in the first year. The more driving experience, the less you pay for car insurance.

- Use the SF classes of scooters and motorcycles. You can transfer the SF classes from motorcycles and scooters with a power of at least 50 cubic centimeters to car insurance. Hence, reducing the insurance cost.

- Transfer the accident-free years from driving someone else’s car to your new vehicle.

- Use telematics tariffs (Telematik Tariff) and save up to 30% in car insurance costs.

- Get third-party liability insurance for older cars

What does good car insurance in Germany cover?

Your car insurance policy should fulfill the five criteria below. Otherwise, you risk poor coverage and financial ruin.

At least 50 million insured sum

The maximum amount the car insurer will cover is very important when taking out car insurance in Germany. If your insured sum is less than 50 million, you may run into financial trouble in case of serious accidents.

Hence, we recommend you buy tariffs that offer at least 50 or 100 million euros as the insured sum.

Mallorca policy

This option is vital if you rent a car in other European countries. Under the Mallorca policy, the insured sum for the rental car in European countries automatically increases to the German level.

Hence, you are well insured for liability when on holiday. The best part is that it doesn’t cost extra.

No plea of gross negligence (Keine Einrede der groben Fahrlässigkeit in German)

Ensure that your auto insurance contains the “no plea of gross negligence” clause. As per this clause, the insurer waives its right to plead gross negligence. In other words, the insurer covers the damages you caused under gross negligence.

Scenarios that come under gross negligence are

- driving at a red light,

- being too fast,

- typing a message on your cell phone, etc.

Statistically, such scenarios are the reasons for most car accidents.

NOTE: Car insurance does not cover cases of driving under the influence of alcohol or drugs or car theft because of gross negligence.

Marten bites and their consequential damage

Martens like to nibble on car hoses and cables, which can lead to expensive damage. So, you should get car insurance that covers damage to hoses, brake lines, and wiring as well as consequential damages.

Extended damage coverage from wild animals

It’s good to have insurance protection for damage caused by accidents with wild animals. This coverage is standard, and everyone in the insurance industry offers it at no extra charge.

However, sometimes insurance companies do not cover accidents involving domestic animals, such as cows, dogs, horses, etc.

Hence, ensure that your vehicle insurance covers accidents involving all types of animals and is not limited to wild animals like deer or wild boar.

What is less important in car insurance in Germany?

Passenger accident insurance (Insassen-Unfallversicherung in German)

Under this tariff, insurance pays the costs arising from the injury or death of the passengers in your car. But the car liability insurance of the person who caused the accident covers these costs.

So, the passenger accident insurance jumps in if the car liability insurance of the person who caused the accident does not cover the damage, for example, a hit-and-run situation.

However, traffic victim assistance (Verkehrsopferhilfe in German) helps in such cases. Hence, making passenger accident insurance useless.

Breakdown insurance (Shutzbriefversicherung)

The breakdown insurance covers the costs when your car breaks down.

The insurer bears the towing costs, may provide a rental car, and may pay for your accommodation when your vehicle is in the workshop.

Some insurers also offer services such as medical evacuation, medicine supply abroad, and payment of funeral or transport costs in the event of death.

If you own a new or well-maintained car, the probability of it breaking down in the middle of nowhere is low. Even if it does, you can pay for the repairs and the towing assistance in most cases.

However, if you still want to protect yourself, you can choose between motor vehicle breakdown insurance or membership in an automobile club like ADAC.

You don’t need breakdown insurance or an automobile club membership for new cars because the manufacturer’s mobility guarantee applies.

What should you do in the event of a car accident in Germany?

If you get in a car accident in Germany, you should ensure that everyone is safe and that medical help (Ambulance phone number 112) is on the way.

Next, you should call the police (phone 110) and report the accident. If you don’t speak German, you can request an English-speaking police officer. But there’s no guarantee that you’ll get one.

Then, collect the following information.

- Personal details like the name and address of the other party involved in the accident.

- The license plate number of the vehicle.

- The third party’s insurer details.

- The exact location of the accident.

- Take a lot of photographs of the accident scene, your car, and the third party’s car.

- Fill out the European accident report (Europäischer Unfallbericht) if another vehicle or person is involved.

You can always contact your car insurance company when in doubt.

What can you do in the event of a hit-and-run?

There might be situations where you have the number plate of the third party and need their insurance details. For example, the other party refuses to provide their insurance details or in a hit-and-run scenario.

In such cases, you can contact Zentralruf der Autoversicherer (the central service center for car insurers) to get the third party’s insurance details.

You can call them or file an inquiry online.

Zentralruf der Autoversicherer maintains the database of every car registered within the EU and Schengen area. So, even if you meet with an accident outside Germany, they can help you with all the relevant information.

You can contact Zentral der Autoversicherer on 0800 250 260 0 (within Germany) and +49 40 300 330 300 (outside Germany). You can reach them 24×7 within Germany. However, only during working days from outside Germany.

As they cover the whole EU, they also speak English. Additionally, they offer free services.

How do you cancel or change your car insurance policy in Germany?

You can cancel or change the car insurance plan in three ways.

- Ask your new car insurance provider to cancel the contract with the old car insurance company. This ensures that your new car insurance policy starts immediately after the old one is canceled.

- Send an email to your car insurance company to cancel the contract. In this case, you must ensure that the new policy starts immediately after the old one ends. Otherwise, there will be a period when you have no car insurance coverage.

- Use comparison portals – Verivox* and Check24*, to cancel or switch your vehicle insurance.

NOTE: You can terminate your motor vehicle insurance immediately after selling your car. The insurance company automatically refunds the premium for the rest of the year to your registered bank account.

When can the insurer deny you the car insurance policy in Germany?

German auto insurance companies must accept car insurance applications under the Compulsory Insurance Act (Section 5/2).

However, the insurance company may refuse to issue a policy under certain circumstances. For example, the applicant violated the terms of the contract with them in the past.

What can you do if the car insurance provider rejects your claim?

You have the following options if the car insurance company rejects your claim.

- Write to your car insurer’s complaints department.

- File a complaint with BaFin. BaFin is the Federal Financial Supervisory Authority of Germany, which ensures companies do not exploit consumers.

- Contact Insurance Ombudsman. They are independent entities that help consumers settle disputes with insurance companies outside of court.

- Sue, the car insurance provider. Legal disputes can be expensive. Thus, having legal insurance in Germany is recommended. Legal insurance (Rechschutzverschierung) covers the cost of legal disputes, such as lawyer and court fees.

Best legal insurance in Germany ->

What is an eVB number in Germany?

When you take out car insurance in Germany, you get an eVB number (Elektronik Versicherungsnummer). An eVB number is proof that you have car insurance.

You need an eVB number when registering your car in Germany. You also need it when you move to a new city and must re-register your car in the new city.

You receive the eVB number via email immediately after concluding the car insurance policy online. Later, you’ll receive the contract and other car insurance documents by post.

Roadside assistance in Germany

If you often travel long distances by car, you should get a roadside assistance service in Germany. The roadside assistance service includes towing your car, repairing it, and offering a hotel stay or ride back home.

Two major players in Germany that offer roadside assistance services are ADAC and AvD. You don’t need their membership if you have a new car or don’t travel long distances often.

Is your German car insurance valid outside Germany?

German car insurance is normally valid in EU member states. However, to confirm, you can ask your car insurance provider to issue you a green card (Grüne Karte).

The green card contains the information about the countries in which your car insurance is valid. If you are traveling to a country where your car insurance is invalid, you must buy one to cover your trip.

If you travel outside Germany often, ensure your car insurance policy has a “Mallorca Policy” clause.

FAQ

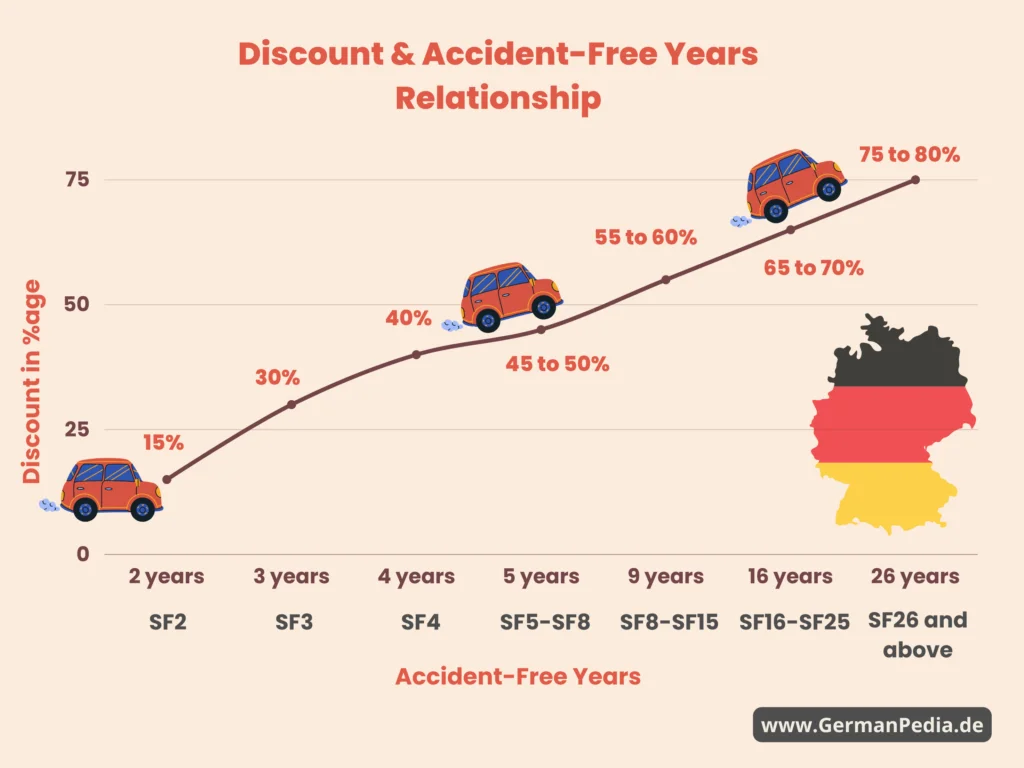

What is Schadensfreiheitsklasse (SF-Klasse)?

English translation of “Schadensfreiheitsklasse” is “class without claims.” It’s an accredit rating system that car insurers in Germany use.

The insurer gives the rating based on the number of accident-free or no-claim years. The rating ranges from SF0 to SF50, with the digit next to “SF” representing the number of accident-free years.

The higher the rating, the lower the vehicle insurance premium. You can also consider it a no-claim bonus that the insurer gives you for not filing the insurance claim.

| Accident-free or no claims years | SF Class (Schadenfreiheitsklasse) | Discount |

|---|---|---|

| 2 years | SF2 | ~15% |

| 3 years | SF3 | ~30% |

| 4 years | SF4 | ~40% |

| 5 to 8 years | SF5 to SF8 | 45 to 50% |

| 9 to 15 years | SF9 to SF15 | 55 to 60% |

| 16 to 25 years | SF16 to SF25 | 65 to 70% |

| 26 years or more | SF26 and above | 75 to 80% |

Do I need insurance to drive a car in Germany?

Yes, every vehicle in Germany must have at least third-party liability car insurance. You cannot drive a car in Germany without car insurance.

Do you insure the car or the driver in Germany?

You can take insurance for both the car and the driver. However, third-party liability insurance doesn’t cover you (the driver) if you cause the accident.

Thus, to cover personal injury, you should take full-comprehensive insurance (vollkasko).

How to get cheap car insurance in Germany?

To get cheap car insurance, compare the tariffs on comparison portals: Verivox* and Check24*.

Are foreign cars more expensive to insure?

Yes, as the spare parts of imported cars are expensive, insurance companies increase the premiums to compensate.

Should I get car insurance from an insurance broker?

You don’t need an insurance broker to find good and cheap motor vehicle insurance in Germany. Instead, compare the tariffs on comparison portals, Verivox* and Check24*, to find the right insurance cover.

The following car insurance plans are rated the best by Germany’s top rating agencies and insurance experts.

- CosmosDirekt (Comfort)*

- HUK24 (Classic with Kaskoplus)

- AXA (Comfort)*

- Allianz (Comfort, Premium)

- DEVK (Komfort-Schutz)

More topics