Key Takeaways

- Foreigners can buy real estate in Germany. There is no visa requirement to buy a house in Germany.

- Foreigners need a valid visa to get a mortgage from a German bank.

- A price atlas from Homeday or Immobilienscout24 will give you a good idea of house prices in a particular location.

- You can negotiate a better mortgage contract if you have offers from different banks in Germany.

- As a buyer, you have the right to choose your Notary. Thus, you can look for an English-speaking Notary.

This is how you do it

- Use real estate portals like immobilienscout24 to find a property within your budget.

- Contact several German banks and brokers to determine how much of a loan you can get and on what terms.

- Get a creditworthiness letter from a German bank to increase your chances of buying a house in Germany.

- You can hire a property appraiser (Gutachter) to evaluate the house you are considering buying in Germany.

- Sign the mortgage contract one week before signing the property purchase contract (Kaufvertrag).

- We have written a book on buying a house in Germany. It explains the complete buying process, how to invest in German real estate, and offers expert tips that'll save your thousands of euros.

Table of Content

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Can foreigners buy property in Germany?

Anyone can buy a property in Germany. You don’t need Germany’s visa to purchase a home in Germany. Thus, foreigners can also buy property if they have the money.

Suppose you don’t have your own cash and require a loan from a bank in Germany. In this case, you need a valid visa (preferably permanent residence). Read our guide on how to get a mortgage in Germany to learn more.

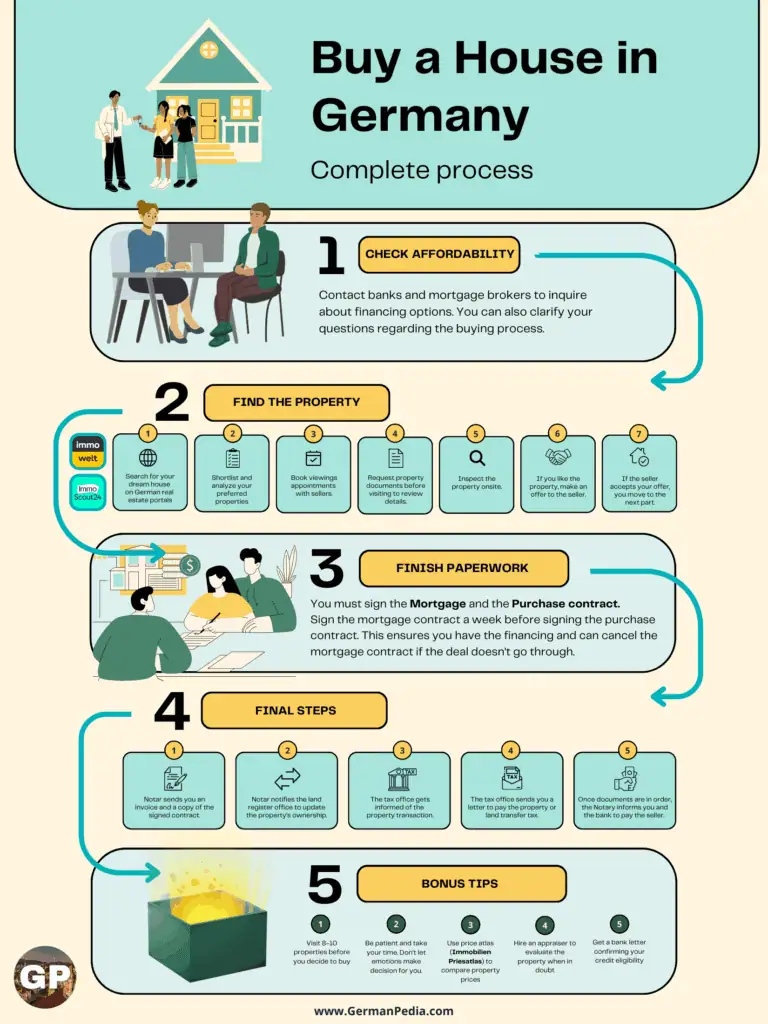

Steps to buying a house in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The home-buying process consists of four parts:

- Checking your affordability

- Finding a property within that range

- Finishing the paperwork required to buy the property

- Waiting period

Step 1: Check your affordability

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The first step is determining your options to finance a property in Germany. To do that, contact brokers and banks to check how much credit you can get.

Contact banks to explore the options for financing a property in Germany

We suggest you contact your home bank first. Ask them how much credit you are eligible for. It’ll give you an idea about the mortgage terms and conditions.

You shouldn’t rely on one bank. You should contact multiple banks instead to know your home financing options.

NOTE: Tell the bank advisor you are here only to make a mortgage inquiry. And it should not affect your SCHUFA score.

Getting financing offers from multiple banks hurts your Schufa score. Thus, ensure that the bank knows you are only enquiring about the mortgage and don’t want an offer.

Contact mortgage advisors or German brokers to explore different mortgage offers.

Contact mortgage brokers in the next step. Here are some of the big players in the market.

Mortgage brokers are affiliated with hundreds of banks and can provide a good market overview.

Note: Never make a buy decision based on a broker’s word. They are only the middle man.

Brokers may say you can get a home loan, but the bank may reject it. Thus, you don’t have a loan until the bank confirms.

Interhyp – Mortgage brokers in Germany

- Offer support in finding the right mortgage product.

- Help you understand the process of buying a property in Germany.

- A mortgage broker can find mortgage options from several banks within minutes.

Dr. Klein – Mortgage brokers in Germany

- Offer support in finding the right mortgage product.

- Help you understand the process of buying a property in Germany.

- A mortgage broker can find mortgage options from several banks within minutes.

The goal of contacting different banks and brokers in the home-buying process

The purpose of contacting various banks and mortgage brokers is to know your affordability. You can also learn a lot about the steps to buy property in Germany from mortgage brokers and bank advisors.

As you are collecting information, don’t focus on negotiating mortgage offers with the banks. It’s something you can do later.

Currently (2024), you have a 100% finance option in Germany. This means you can get a loan that is equal to the property’s purchase price.

However, you must pay the Nebenkosten (Property purchase cost) from your pocket. Cost of buying a house in Germany is between 7% and 12% of the property’s price.

By the end of this step, you’ll know how much you can afford and how much you need to bring from your side.

Once you know your price range, it is time to start looking for a property.

Step 2: Find the right property in Germany

You must spend some time researching Germany’s property market to find your dream house. An advertisement can tell you a lot about a property.

The more properties you browse online, the better you’ll understand the housing market in Germany.

Steps from searching for a property to sending an offer to the seller

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Start searching for your dream house on German real estate portals.

- Analyze the properties you like online and shortlist the ones that look interesting.

- Book an appointment with the sellers to visit those properties.

- Ask the seller to send you the property documents before your visit. This will allow you to study the documents and learn more about the property before visiting.

- Inspect the property onsite.

- If you like the property after your visit, you can make an offer to the seller.

- If the seller accepts your offer, congratulations, you move to the next part.

Major real estate websites you can use for finding a property in Germany

- Immobilienscout24

- Immowelt

- eBay kleinanzeige

- Banks’ websites (e.g., Post bank, BW bank, Sparkasse, etc.): Different banks also have websites to sell houses. They post the latest homes available for sale on their websites first. Hence, it’s worth looking there also.

- Local newspaper: Germany has an aging population. The baby boomer generation still prefers using newspapers to post advertisements.

TIP: You can find some great deals by browsing local newspapers. You get these newspapers for free in your post box. Simply look for the section “Immobilien” to find the properties on sale.

Tips and Recommendations on Buying Real Estate in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

- Visit at least eight to ten properties before you decide to buy one.

- The more properties you see, the more you’ll learn about your local real estate market.

- Don’t be in a hurry to buy a house. Finding the right property is a time-consuming process. Moreover, buying a property is one of the major financial decisions of your life.

- Use the price atlas from Immobilienscout24 and Homeday to understand the property prices in a particular area.

- Suppose you are confused and cannot evaluate a property yourself. Then, you can hire an “Appraiser (Gutachter or Sachverständiger)” to evaluate the house you want to buy. To find one, Google “Gutachter <Your city name>” or “Sachverständiger <Your city name>.”

- Get a letter from the bank stating that you are eligible for up to X amount of credit. It’ll tremendously increase your odds of getting the property in a competitive real estate market. Unfortunately, many people either don’t know about it or don’t use it.

Free Download Property Inspection Checklist

- Download the checklist for things you should inspect while visiting a property in Germany.

- Know the documents you need from the seller.

Step 3: Paperwork required to buy a house in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

You have found your dream home, and the seller agreed to your offer. The next step is to check the paperwork you must do to become a homeowner.

Mortgages in Germany: Get the mortgage contract from a German bank

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Here are the steps to get a mortgage in Germany.

- Get a list of documents: Contact your bank and get a list of documents they require to give you credit.

- Submit the required documents to the bank. Once you have submitted all the required documents, the bank may take some time to check them.

- The bank might send an appraiser to evaluate the property. The appraiser’s job is to check if the house price is fair. Every bank evaluates the property differently. The property price banks come up with is usually lower than the sale price. But, in most cases, the bank’s lower house valuation is not a major concern.

- After evaluating the property and your profile, the bank will make you a final offer. The bank will draft a mortgage contract if you agree to the offer.

- You must negotiate the mortgage offer with the banks. You can negotiate the terms successfully if you have offers from other banks. Learn the tricks to negotiating an offer with a German bank here.

- Finalize the bank: This step ends once you finalize the bank and sign the mortgage contract.

NOTE: Always compare the total loan cost instead of the interest rate when getting a mortgage in Germany. Different banks calculate interest differently, which may lead to higher or lower loan costs. Additionally, some banks force their customers to take residual debt insurance, hence increasing the loan cost.

Read our guide on mortgages in Germany to learn how to get a mortgage as an expat.

How to get the best mortgage offer in Germany?

- Tips and tricks for financing a property in Germany.

- Learn the German vocabulary to find the best mortgage in Germany.

- Documents required to get finance a house in Germany

Find the notary to formalize the home-buying process

Once you have a final mortgage offer from the bank, the next step is to look for a notary (Notar) near you and book an appointment.

Who is a Notary (Notar)?

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

A notary (Notar) is a neutral entity that drafts the purchase contract (Kaufvertrag in German). It considers both the seller’s and the buyer’s interests.

Notar has the following responsibilities.

- It ensures that the seller can sell the property.

- It informs the buyer about the property’s use restrictions, if any.

- Informs you (buyer) when to pay the purchase price to the seller.

- Informs the tax office and property registration office about the property sale.

In short, Notar takes care of the whole buying process and protects both buyers’ and sellers’ interests.

Do I have the freedom to choose my Notary?

As a buyer, you have the right to choose your Notary. Thus, if you are looking for an English-speaking Notary, you have a chance to find one.

In big German cities, it’s easy to find an English-speaking Notary. But you don’t have to worry if you cannot find one. You can hire a translator to translate the proceedings and the documents.

NOTE: If you hire a translator for your meetings with the Notar, you must also bring the translator to your bank appointments. This is a must, as per German law.

Another alternative is to verify the purchase contract by an English-speaking lawyer. The lawyer can inform you if something needs to be changed in the contract.

The initial draft of the purchase contract (Kaufvertrag in German)

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Once you have found the Notary, it’s time to book an appointment with them.

The notary will ask you to complete a two-page form requesting buyers’, sellers’, and property information. The notary needs this information to create the initial draft of the purchase contract.

Once the draft is ready, the Notary will send it to both buyer and seller at least two weeks before signing the contract. This gives the buyer and seller enough time to review the contract.

You can review the contract yourself, with a lawyer, or with a friend.

If you want to make any changes to the draft, you can ask the Notary. Once both parties agree to its conditions, the notary creates the final contract.

Sign the Mortgage and Purchase Contract to finalize the property purchase in Germany

By this time, both mortgage and purchase contracts are ready. The next step is to make appointments with the Notary and the bank to sign the contract.

💡 TIP: You should sign the mortgage contract before signing the purchase contract.

There are two reasons behind it:

- First, it ensures you have the money before signing the purchase contract.

- Second, you can cancel the mortgage contract if you or the seller decides to cancel the deal at the last moment.

You can cancel the mortgage contract without charges within 14 days in Germany.

💡 NOTE: 14 days include weekends and public holidays. So, do not confuse them with business days. When in doubt check with your bank consultant.

Once you have signed the mortgage contract, it’s time to sign the purchase contract. The signing of the purchase contract marks the end of this part. It’s also the last big step from your end.

Step 4: Final steps toward homeownership in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

Congratulations, you have done all the hard work, and now it’s time to sit back and wait. From this point onward, you follow the instructions of the Notary. Here is what will happen next.

- Notar will send you the invoice for their services and a copy of the signed purchase contract.

- Notar will notify the land register office (Grundbuchamt) to add your name as a new homeowner.

- The tax office (Finanzamt) gets notified about the property transaction.

- Finanzamt sends you (the buyer) a letter to pay the property transfer tax or land transfer tax (Grunderwerbsteuer). It may take a month from signing the purchase contract or longer to receive this letter.

- The Notary ensures all the documentation is in order. If yes, Notar will inform you and the bank to pay the seller the agreed purchase price.

Once you have paid the purchase price, congratulations; you are the house owner in Germany. Not officially, but you get the keys and can move into your new house or rent it out.

You officially become the owner when your name is entered in the land registry. However, the land register office usually takes 2–3 months to enter the new owner’s name.

I know it’s a lot, but the hard part from your end is to find the right home and credit. After that, the rest falls into place.

You now have an overview of the home-buying process in Germany. To dive deep into each step, check our guides.

- How do you find a good Mortgage in Germany?

- Understanding property documents

- Evaluating property online

- Evaluating property onsite

Buying a home in Germany is time-consuming and involves a lot of money. There are a lot of things you must know before buying a property.

Thus, we wrote a book on buying a house in Germany to make it simple for you. Read it to learn everything there is about buying a property in Germany.

Master German Home Buying Process

in 12 Days For FREE

- Learn complete process of buying a house in Germany and how to invest in German real estate.

- Understand mortgage process, property documents and evaluation, and more.

- Expert tips that’ll save you thousands of euros.

- Know average renovation costs in Germany to plan and negotiate better.

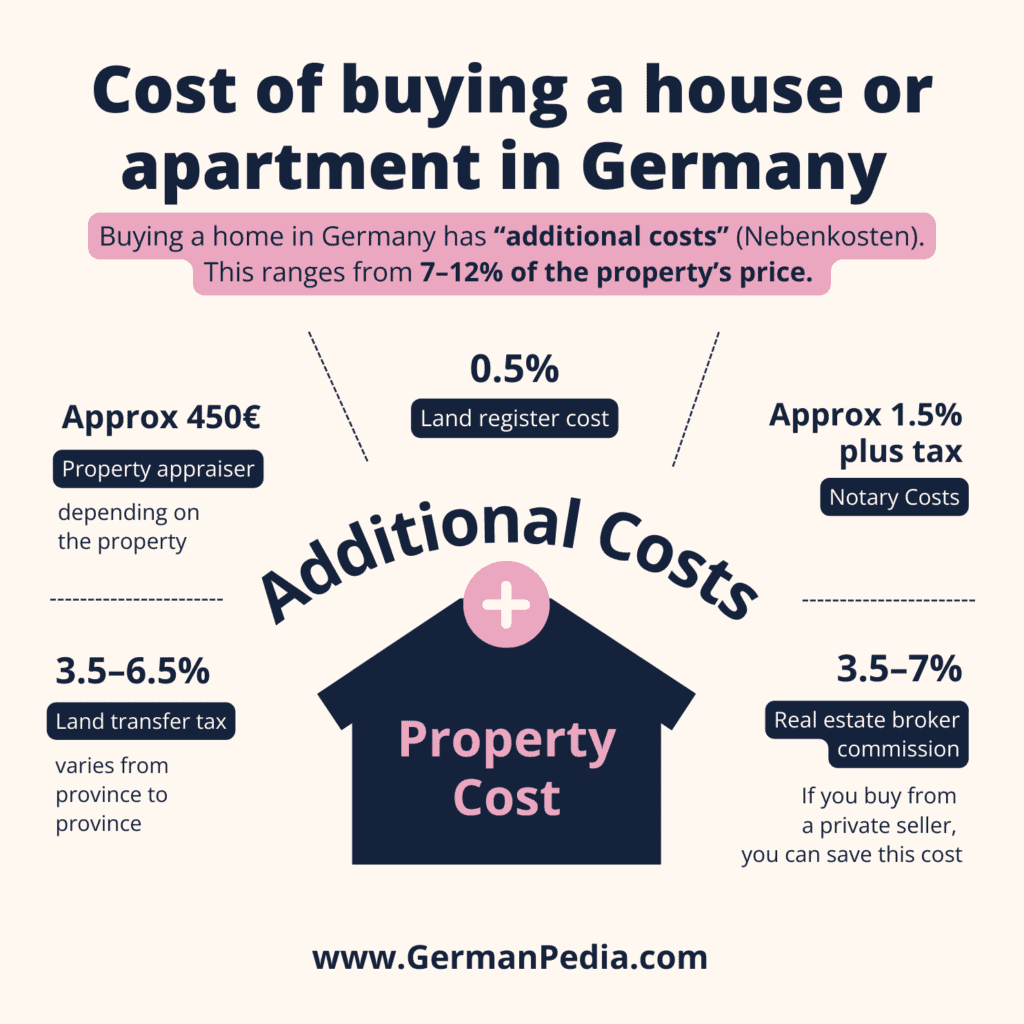

Cost of buying a house or apartment in Germany (Nebenkosten)

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The cost of buying a home in Germany is between 7% and 12% of the property’s price. This is known as Nebenkosten in German.

The table below shows the costs of buying a house in Germany.

| Expenses involved in buying a house in Germany | How much does it cost? |

|---|---|

| Land transfer tax (Grunderwerbsteuer) | 3,5 – 6,5 % (varies from province to province) |

| Land register cost (Grundbuchkosten) | 0,5% |

| Notary Costs (Notarkosten) | Approx 1,5 % plus tax |

| Real estate broker commission (Maklergebühren) | 3,5 – 7 % (If you buy from a private seller, you can save this cost) |

| Property appraiser (Gutachter/Sachverständiger) | Approx 450 €, depending on the property |

The cost of buying a house (Nebenkosten) is the sum you need on top of the real estate’s sale price. For example, you want to buy an apartment that costs 250,000€. You need between 17.5k (7% of 250k) and 30k (12% of 250k) from your pocket.

Thus, the total cost to buy the apartment is 250k € + (17.7k to 30k) €.

The cost of buying a house in Germany depends on two factors:

- Land transfer tax in the province where you buy a house

- Real estate broker’s commission.

Different provinces of Germany have varying land transfer taxes. Similarly, different brokers charge different commissions.

You’ll save thousands of euros if you do not buy the property via a real estate agent. The table below summarizes the land transfer tax in different provinces of Germany.

| Province | Land transfer tax |

|---|---|

| Bayern | 3,5 % |

| Baden-Württemberg | 5,0 % |

| Bremen | 5,0 % |

| Berlin | 6,0 % |

| Brandenburg | 6,5 % |

| Hamburg | 5,5 % |

| Hessen | 6,0 % |

| Mecklenburg-Vorpommern | 6,0 % |

| Niedersachsen | 5,0 % |

| Nordrhein-Westfalen | 6,5 % |

| Rheinland-Pfalz | 5,0 % |

| Saarland | 6,5 % |

| Sachsen | 5,5% |

| Sachsen-Anhalt | 5,0% |

| Schleswig-Holstein | 6,5% |

| Thüringen | 5,0% |

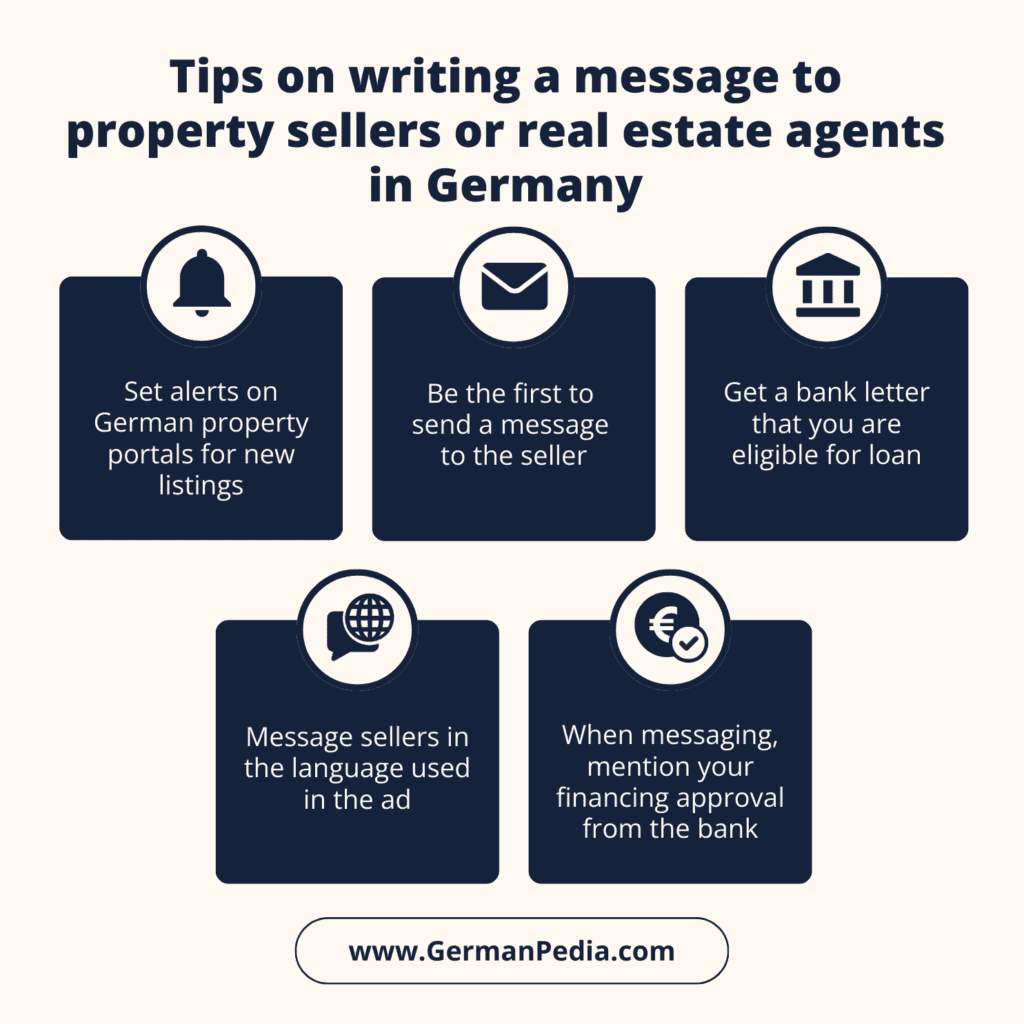

Tips on writing a message to property sellers or real estate agents in Germany

Use this Visualization: You may use this image for free with proper attribution to GermanPedia (i.e., by linking back to GermanPedia).

The gap between the supply and demand of real estate in Germany is high. Because of this, the property seller gets a lot of requests from potential buyers. Thus, do the following to get your foot in the door.

- Set notification alerts on the German property portals to get an email when someone posts a new property.

- Be the first to send a message to the seller. After browsing and visiting enough properties, you can judge a new one within minutes.

- Get a creditworthiness letter from the bank stating you are eligible to get a loan of X amount.

- Write the message in the language used in the advertisement. For example, if the ad is in German, write the message in German.

- Always mention in your message that you have financing approval from the bank.

Here is a sample message you can write to the property seller.

Hallo Herr/Frau <Last name of the seller>,

ich interessiere mich für die Wohnung. Ich habe die Finanzierung von der Bank. Können Sie mir bitte einen Termin geben, um die Wohnung zu besuchen?

Viele Grüße,

<Your name>

<Your contact information>

Is it better to buy or rent a house in Germany?

Many struggle with the question of whether to buy or rent a house. There is no simple way to answer it.

However, if you can afford buying a house, you should buy it. Statistically speaking real estate is the best hedge against inflation.

Moreover, you can get a 100% mortgage, which makes buying a house even more attractive. You can contact mortgage brokers for unbinding loan offers. We have worked with Finance for Expats* for quite some time and highly recommend them.

Generally speaking, renting a place makes more sense in the following scenarios.

- You have other responsibilities and debt, which makes owning a property tough.

- You want to start your own business.

- You don’t have a stable income.

Why is the homeownership percentage low in Germany?

As of 2023, only 47.6% of Germans own a house. Compared to other European countries, Germany has the lowest homeownership percentage. [3]

Several factors contribute to the low ownership number.

- Affordable rents: In Germany, apartments and houses have long been affordable to rent. However, this has changed in the past few years, and the rent has increased drastically.

- Germany has tenant-friendly laws. For example

- The landlord needs a very strong reason to cancel the rental contract.

- The landlord cannot increase rent by more than 20% (15% in some federal states) within three years.

- The notice period to vacate a rental property is based on how long you have lived there. The longer you live in a property, the longer the notice period.

- Several government policies also make homeownership unattractive.

- High real estate transfer tax. The real estate transfer tax in Germany is between 5 and 6.5%, which is very high compared to just 0.33% in the USA.

- No tax advantages: If you live in the property yourself, you cannot deduct the mortgage interest from the tax.

- Low income: The average gross annual income of full-time employees in Germany varies between 26,820 € and 81,929 €, with an average of 54,163 € (as of 24 March 2022). On the other hand, property prices in Germany have more than doubled since 2003 [4]. The median price of a 2-room apartment in Germany is 5,123 € per m2 (as of Apr. 2024). So, high property prices and low salaries make buying a house tough [5].

How high are the property prices in Germany?

Property prices in Germany have more than doubled since 2003. They have come down by 25% since Q2 2022. But still 50% higher since 2015. [7]

Here are the median property prices in the German federal states.

| City | Apartment price (per m2) | House price (per m2) |

| Berlin | 8,375 € | 6,523 € |

| Nordrhein-Westfalen | 3,156 € | 3,008 € |

| Baden-Württemberg | 4120 € | 3276 € |

| Bayern | 4038 € | 3654 € |

| Hessen | 3900 € | 2543 € |

| Brandenburg | 5238 € | 5067 € |

| Rheinland-Pfalz | 3446 € | 2239 € |

| Niedersachsen | 3392 € | 2206 € |

| Sachsen | 3129 € | 1725 € |

| Schleswig-Holstein | 3640 € | 3148 € |

| Hamburg | 5393 € | 5274 € |

| Sachsen-Anhalt | 2281 € | 1557 € |

Is it okay to buy an old property in Germany?

When you look for apartments and houses in Germany, you’ll see that many properties were constructed in the 1960s. It’s normal to question whether you should buy an apartment in a 65-year-old building or not.

The answer to this question is YES. German properties are very well-constructed, and Germans take pride in their houses’ strength. So, you don’t have to worry about buying an apartment in a well-maintained 70-year-old building.

Due to a shortage of houses in Germany, many new building projects are underway. New buildings are modern and energy efficient, but they are more expensive than older ones.

How much down payment must you bring to buy a house in Germany?

You don’t need to make a down payment to get a mortgage in Germany. German banks offer 100% financing. However, you must cover the costs of buying a house in Germany, also known as Nebenkosten.

The cost of buying a house in Germany is between 7% and 12% of the purchase price.

There are several advantages of making a down payment.

- Your chances of getting a mortgage increase.

- You get better interest rates.

- You can get a higher loan amount.

In short, the more down payment you bring, the better the mortgage conditions you get.

More topics

References

- https://www.dbresearch.com/PROD/RPS_EN-PROD/PROD0000000000527713/2023_Housing_market_outlook%3A_Price_dip_and_interes.PDF

- https://ec.europa.eu/eurostat/databrowser/view/ILC_LVHO02__custom_3462892/bookmark/table?lang=en&bookmarkId=bf0879f1-9638-4868-8d59-5800871c15aa

- https://www.bundesbank.de/en/publications/research/research-brief/2020-30-homeownership-822176